Each week, we tap the insight of Sam Stovall, Chief Investment Strategist, CFRA, for his perspective on the current market.

EQ: After a strong start to the year, stocks seem to have lost their footing a bit, closing out the first quarter of 2018 in the red nearly across the board. What kind of implications could this have for the rest of the year?

Stovall: I think the market’s activity in the first quarter gives us a pretty clear clue as to what might happen for the remaining quarters of the year, which is an increase in volatility. In 2017, the S&P 500 experienced only eight days in which it rose or fell by 1% or more. Through the first quarter of 2018, we’ve had 25 such days, essentially nearly 100 times on an annualized basis. Volatility is back, and I think that’s what the market is telling us.

Furthermore, at least in the past couple of months, we’ve seen a self-righting mechanism kick in as it relates to the stock valuations. Valuations were stretched by the end of January, but now they’ve come back into more normal areas. The S&P 500 was trading at 19 times 2018 earnings estimates but is now trading at close to 16.5 times. Technology, which was at 20 times, fell to about 17.5 times.

EQ: There are a number of significant headwinds and concerns that investors are facing right now. However, one catalyst that bulls are pointing to is the upcoming earnings season to help stabilize the markets. You discussed valuations having been stretched earlier in the year, but how could a strong earnings period get the market back on track?

Stovall: Well, first quarter earnings are expected to be up 16.6% for the S&P 500. In addition, eight of the 11 sectors are expected to post double-digit increases. For the full year, the S&P 500 is likely to see more than 18.5% in earnings growth. So, how do you forecast a recession when earnings are expected to be that strong?

I think that has provided a bit of comfort for investors who are worried about recent market activity, because even though we do have a significant number of headwinds—in particular, Tech and trade—the fundament backdrop remains fairly healthy, and that should allow us to weather the near-term storm.

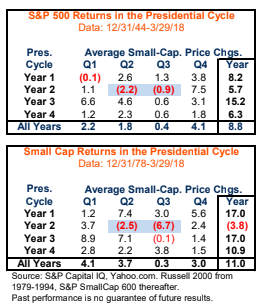

EQ: In this week’s Sector Watch, you looked at the market’s historical performances during mid-term election years. Considering 2018 is one them, and the amount of uncertainty surrounding the current political climate, how cautious should investors be from now until November?

Stovall: I think they should simply be aware that we are approaching a very challenging period for stocks. The second and third quarters of mid-term election years are by far the worst quarters of the entire 16-quarter presidential cycle. On average, the second quarter is down 2.2% and the third quarter is down approximately 1%. For comparison, the next worst performance was down only 0.1% on average.

So, the next two quarters are going to be challenging simply because of one word: uncertainty. That’s particularly as to the makeup of Congress once mid-term elections have run their course. Right now, a lot of the political pundits are saying that they think that there is a very good chance the Republicans will lose control of the House of Representatives, and that could throw us back into another gridlocked situation.

EQ: With that being said, it looks as though investors may be able to take some solace in knowing that the quarters after the midterm elections are over typically have been quite strong for the market. How have stocks performed in that period historically?

Stovall: That’s a very good point because, since World War II, there have been 18 midterm elections, and the market was up 18 of 18 times in the 12 months after those midterm elections, gaining an average of 16.5%. There’s no guarantee that will happen this time, but essentially, what it says is, once you get this uncertainty out of the way, Wall Street can continue on the way it normally does.

EQ: You also found that there were 12 sub-industry groups that have managed to produce positive returns during this upcoming turbulent period. Why do you think these groups in particular have been able to outperform more times than not in this type of environment?

Stovall: It is sort of interesting because when you go all the way back to WWII and you’re looking exclusively at the second quarter, a lot of that probably has to do with luck. Basing it on how the economy was growing and what phase of the economic and stock market cycle we were in, I don’t think a lot of it has to do with the political issues being batted about. However, usually it is those areas where Americans have been known to frequent quite a bit.

Whether it’s looking at Brewers/Distillers & Vintners, or Soft Drinks and Tobacco, it’s in a sense your more defensive areas. It may also happen to do with Americans and their love affair with automobiles, because the Auto Manufacturers have done well. In addition, knowing that a strong national defense is one that every politician tends to support, and it’s not surprising that Aerospace and Defense has done relatively well too. I think in all, a lot of it has to do with defensiveness, combined with what Americans by nature tend to embrace.