In April of 2018, I wrote an article entitled “10-Reasons The Bull Market Ended In 2018” in which I concluded:

“There is a reasonably high possibility, the bull market that started in 2009 has ended. We may not know for a week, a month or even possibly a couple of quarters. Topping processes in markets can take a very long time.

If I am right, the conservative stance and hedges in portfolios will protect capital in the short-term. The reduced volatility allows for a logical approach to further adjustments as the correction becomes more apparent. (The goal is not to be forced into a ‘panic selling’ situation.)

If I am wrong, and the bull market resumes, we simply remove hedges and reallocate equity exposure.

‘There is little risk, in managing risk.’

The end of bull markets can only be verified well after the fact, but therein lies the biggest problem. Waiting for verification requires a greater destruction of capital than we are willing to endure.”

It is important to remember, that “Risk” is simply the function of how much you will lose when you are wrong in your assumptions.

2018 has been a year of predictions gone horribly wrong.

Not surprisingly, after a decade-long bull market, individuals who were betting on a more positive outcome this year are now clinging to “hope.”

Do you remember all of the analysis about how:

- Rate hikes won’t matter

- Surging earnings due to tax cuts will power the market higher

- Valuations are reasonable

These were all issues which we have heavily questioned over the last couple of years.

And the majority of our warnings “fell on deaf ears” as just being simply “bearish.”

Of course, you really can’t blame the average investor for ignoring fundamental realities considering they have been repeatedly told the stock market is a “sure thing.” Just “buy and hold” and the market will return 10% a year just as it has over the last 100 years.

This fallacy has been so repeatedly espoused by pundits, brokers, financial advisors, and the media that it has become accepted as “truth.”

But, if it were true, then explain why roughly 80% of Americans, according to numerous surveys, have less than one years salary saved up on average? Furthermore, no one who simply bought and held the S&P 500 has ever lost money over a 10- or 20-year time span. Right?

Not exactly.

Here is the problem.

No matter how resolute people think they are about buying and holding, they usually fall into the same old emotional pattern of “buying high” and “selling low.”

Investors are human beings. As such, we gravitate towards what feels good and we seek to avoid pain. When things are euphoric in the market, typically at the top of a long bull market, we buy when we should be selling. When things are painful, at the end of a bear market, we sell when we should be buying.

In fact, it’s usually the final capitulation of the last remaining “holders” that sets up the end of the bear market and the start of a new bull market. As Sy Harding says in his excellent book “Riding The Bear:”

“No such creature as a ‘buy and hold’ investor ever emerged from the other side of the subsequent bear market.”

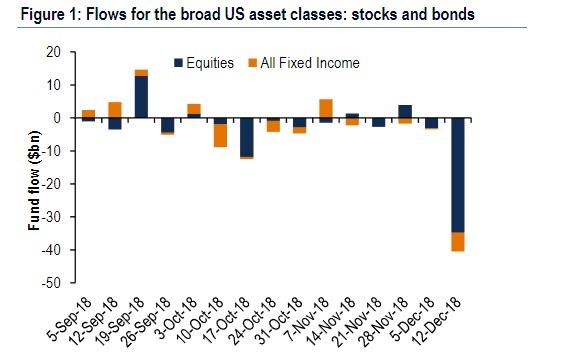

Statistics compiled by Ned Davis Research back up Harding’s assertion. Every time the market declines more than 10%, (and “real” bear markets don’t even officially begin until the decline is 20%), mutual funds experience net outflows of investor money. To wit:

“Lipper also found the largest outflows on record from stocks ($46BN), the largest outflows since December 2015 from taxable bond ($13.4BN) and Investment Grade bond ($3.7BN) funds, and the 4th consecutive week of outflows from high yield bonds ($2.1BN), offset by a panic rush into cash as money market funds attracted over $81BN in inflows, the largest inflow on record.”

“Fear is a stronger emotion than greed.”

Most bear markets last for months (the norm), or even years (both the 1929 and 1966 bear markets), and one can see how the torture of losing money week after week, month after month, would wear down even the most determined “buy and hold” investor.

But the average investor’s pain threshold is a lot lower than that. The research shows that it doesn’t matter if the bear market lasts less than 3 months (like the 1990 bear) or less than 3 days (like the 1987 bear). People will still sell out, usually at the very bottom, and almost always at a loss.

So THAT is how it happens.

And the only way to avoid it – is to avoid owning stocks during bear markets. If you try to ride them out, odds are you’ll fail. And if you believe that we are in a “New Era,” and that bear markets are a thing of the past, your next of kin will have our sympathies.

But you can do something about it.

Just like any “detox” program, these are the steps to follow to becoming a better long-term investor.

10-Step Process To Curing The Addiction

STEP 1: Admitting there is a problem

The first step in solving any problem is to realize that you have a “trading” problem. Be willing to take the steps necessary to remedy the situation

STEP 2: You are where you are

It doesn’t matter what your portfolio was in March of 2000, March of 2009, or last Friday. Your portfolio value is exactly what it is, rather it is realized or unrealized. The loss is already lost, and understanding that will help you come to grips with needing to make a change. Open those statements and look at them – shock therapy is usually effective in bringing about awareness.

STEP 3: You are not a loser

Most people have a tendency to believe that if they “sell a loser,” then they are a “loser” by extension. They try to ignore the situation, or hide the fact they lost money, which in turn causes more mistakes. This only exacerbates the entire problem until they then try to assign blame to anyone and anything else.

You are not a loser. You made an investment mistake. You lost money.

It has happened to every person that has ever invested in the stock market, and there are many others who lost more than you.

STEP 4: Accept responsibility

In order to begin the repair process, you must accept responsibility for your situation. It is not the market’s fault. It is not your advisor’s or money manager’s fault, nor is it the fault of Wall Street.

It is your fault.

Once you accept that it is your fault and begin fixing the problem, rather than postponing the inevitable and suffering further consequences of inaction, only then can you begin to move forward.

STEP 5: Understand that markets change

Markets change due to a huge variety of factors from interest rates to currency risks, political events, to geo-economic challenges.

If this is a true statement, then how does it make sense to buy and hold?

If markets are in a constant state of flux, and your portfolio remains in a constant state, then the law of change must apply:

The law of change: Change will occur and the elements in the environment will adapt or become extinct and that extinction in and of itself is a consequence of change.

Therefore, if you are a buy and hold investor then you have to modify and adapt to an ever-changing environment or you will become extinct.

STEP 6: Ask for help

This market has baffled, and confused, even the best of investors and will likely continue to do so for a while. So, what chance do you have doing it on your own?

Don’t be afraid to ask, or get help, if you need it. This is no longer a market which will forgive mistakes easily and while you may pay a little for getting help, a helping hand may keep you from making more costly investment mistakes in the future.

STEP 7: Make change gradually

No one said that change was going to easy or painless. Going against every age-old philosophy and piece of advice you have ever been given about investing is tough, confusing and froth with doubt.

However, make changes gradually at first – test the waters and measure the results. For example, sell the positions that are smallest in size with the greatest loss. You will make no noticeable change in the portfolio right away, but it will make you realize that you can actually execute a sell order without suffering a negative consequence.

Gradually work your way through the portfolio on rallies and cleanse the portfolio of the evil seeds of greed that now populate it, and replace them with a garden of investments that will flourish over time.

STEP 8: Develop a strategy

Now that you have cleaned everything up you should be feeling a lot more in control of your portfolio and your investments. Now you are ready to start moving forward in the development of a goal-based investment strategy.

If your portfolio is a hodge-podge of investments, then how do you know whether or not your portfolio will generate the return you need to meet your goals. A goal-based investment strategy builds the portfolio to match investments, and investment vehicles, in an orderly structure to deliver the returns necessary with the least amount of risk possible. Ditch the benchmark index and measure your progress against your investment destination instead.

STEP 9: Learn it. Live it. Love it.

Once you have designed the strategy, including monthly contributions to the plan, it is time to implement it. This is where the work truly begins.

- You must learn the plan inside and out so every move you make has a reason and a purpose.

- You must live the plan so that adjustments are made to the plan, and the investments, to match performance, time and value horizons.

- Finally, you must love the plan so that you believe in it and will not deviate from it.

It must become a part of your daily life, otherwise, it will be sacrificed for whims and moments of weakness.

STEP 10: Live your life

That’s it.

You are in control of your situation rather than the situation controlling you.

The markets will continue to remain volatile as a more important “bear market” takes hold in the next year or so.

The good news is that there will be lots of opportunities to make money along the way.

But that is just how it works. As long as you work your plan, the plan will work for you, and you will reach your goals…eventually.

There is no “get rich quick” plan.

So, live your life, enjoy your family, and do whatever it is that you do best. Most importantly, make your portfolio work as hard for you as you did for the money you put into it.