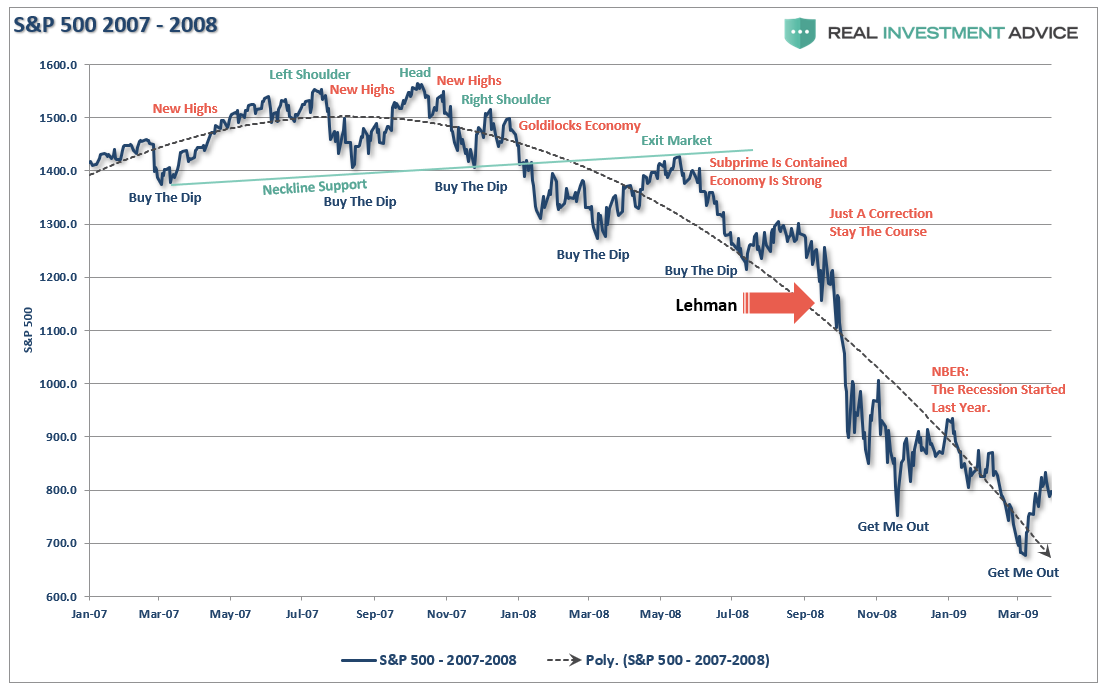

This past week marked the 10th-Anniversary of the collapse of Lehman Brothers. Of course, there were many articles recounting the collapse and laying blame for the “great financial crisis” at their feet. But, as is always the case, an “event” is always the blame for major reversions rather than the actions which created the environment necessary for the crash to occur. In the case of the “financial crisis,” Lehman was the “event” which accelerated a market correction that was already well underway.

I have noted the topping process and the point where we exited the markets. Importantly, while the market was giving ample signals that something was going wrong, the mainstream analysis continued to promote the narrative of a “Goldilocks Economy.” It wasn’t until December of 2008, when the economic data was negatively revised, the recession was revealed.

Of course, the focus was the “Lehman Moment,” and the excuse was simply: “no one could have seen it coming.”

But many did. In December of 2007 we wrote:

“We are likely in, or about to be in, the worst recession since the ‘Great Depression.’”

A year later, we knew the truth.

Throughout history, there have been numerous “financial events” which have devastated investors. The major ones are marked indelibly in our financial history: “The Crash Of 1929,” “The Crash Of 1974,” “Black Monday (1987),” “The Dot.Com Crash,” and the “The Financial Crisis.”

Each of these previous events was believed to be the last. Each time the “culprit” was addressed and the markets were assured the problem would not occur again. For example, following the crash in 1929, the Securities and Exchange Commission, and the 1940 Securities Act, were established to prevent the next crash by separating banks and brokerage firms and protecting against another Charles Ponzi. (In 1999, legislation was passed to allow banks and brokerages to reunite. 8-years later we had a financial crisis and Bernie Madoff. Coincidence?)

In hindsight, the government has always acted to prevent what was believed to the “cause” of the previous crash. Most recently, Sarbanes-Oxley and Dodd-Frank legislations were passed following the market crashes of 2000 and 2008.

But legislation isn’t the cure for what causes markets to crash. Legislation only addresses the visible byproduct of the underlying ingredients. For example, Sarbanes-Oxley addressed the faulty accounting and reporting by companies like Enron, WorldCom, and Global Crossing. Dodd-Frank legislation primarily addressed the “bad behavior” by banks (which has now been mostly repealed).

While faulty accounting and “bad behavior” certainly contributed to the end result, those issues were not the causeof the crash.

Recently, John Mauldin addressed this issue:

“In this simplified setting of the sandpile, the power law also points to something else: the surprising conclusion that even the greatest of events have no special or exceptional causes. After all, every avalanche large or small starts out the same way, when a single grain falls and makes the pile just slightly too steep at one point. What makes one avalanche much larger than another has nothing to do with its original cause, and nothing to do with some special situation in the pile just before it starts. Rather, it has to do with the perpetually unstable organization of the critical state, which makes it always possible for the next grain to trigger an avalanche of any size.“

While the idea is correct, this assumes that at some point the markets collapse under their own weight when something gives.

I think it is actually a little different. In my view, ingredients like nitrogen, glycerol, sand, and shell are mostly innocuous things and pose little real danger by themselves. However, when they are combined together, and a process is applied to bind them, you make dynamite. But even dynamite, while dangerous, does not immediately explode as long as it is handled properly. It is only when dynamite comes into contact with the appropriate catalyst that it becomes a problem.

“Mean reverting events,” bear markets, and financial crisis, are all the result of a combined set of ingredients to which a catalyst was applied. Looking back through history we find similar ingredients each and every time.

The Ingredients

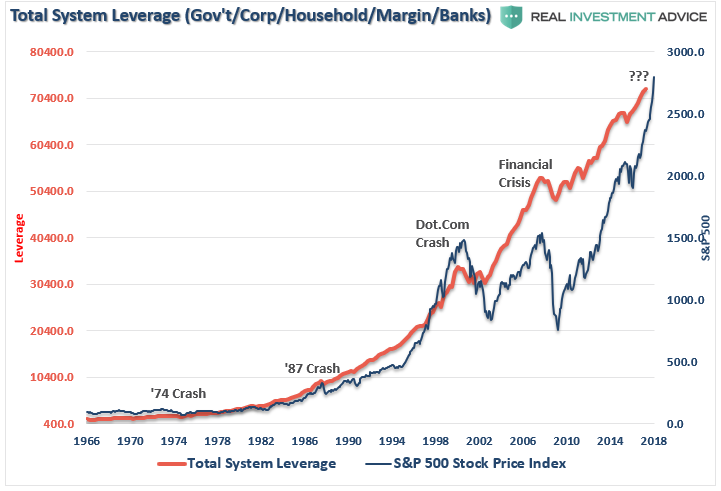

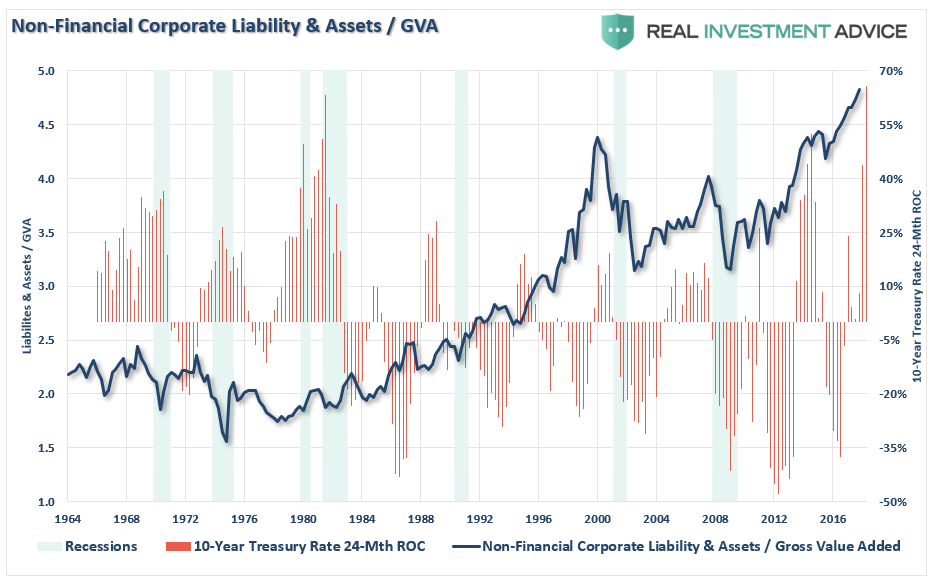

Leverage

Throughout the entire monetary ecosystem, there is a consensus that “debt doesn’t matter” as long as interest rates remain low. Of course, the ultra-low interest rate policy administered by the Federal Reserve is responsible for the “yield chase” and has fostered a massive surge in debt in the U.S. since the “financial crisis.”

Importantly, debt and leverage, by itself is not a danger. Actually, leverage is supportive of higher asset prices as long as rates remain low and the demand for, rates of return on, other assets remains high.

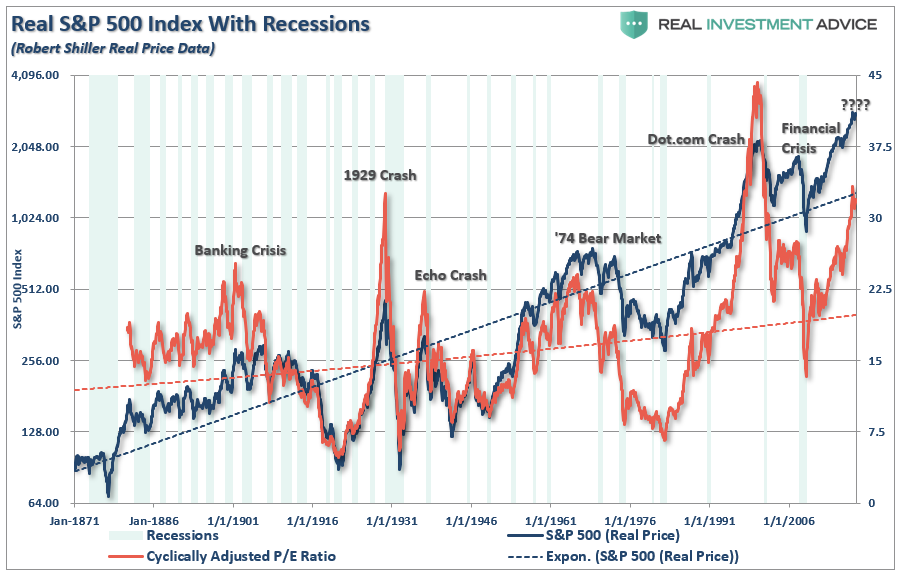

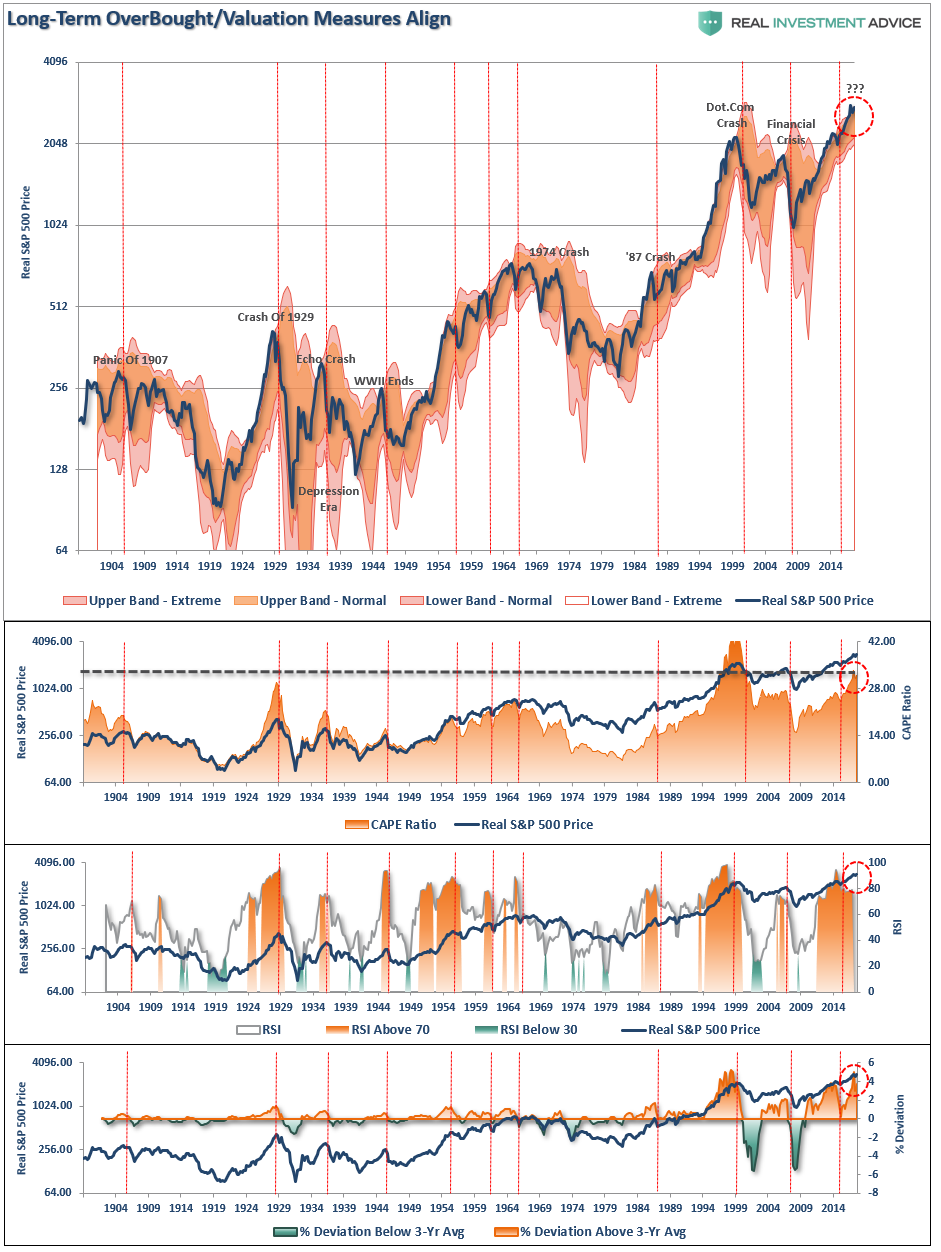

Valuations

Likewise, high valuations are also “inert” as long as everything asset prices are rising. In fact, rising valuations supports the “bullish” thesis as higher valuations represent a rising optimism about future growth. In other words, investors are willing to “pay up” today for expected further growth.

While valuations are a horrible “timing indicator” for managing a portfolio in the short-term, valuations are the “great predictor” of future investment returns over the long-term.

Psychology

Of course, one of the critical drivers of the financial markets in the “short-term” is investor psychology. As asset prices rise, investors become increasingly confident and are willing to commit increasing levels of capital to risk assets. The chart below shows the level of assets dedicated to cash, bear market funds, and bull market funds. Currently, the level of “bullish optimism” as represented by investor allocations is at the highest level on record.

Again, as long as nothing adversely changes, “bullish sentiment begets bullish sentiment” which is supportive of higher asset prices.

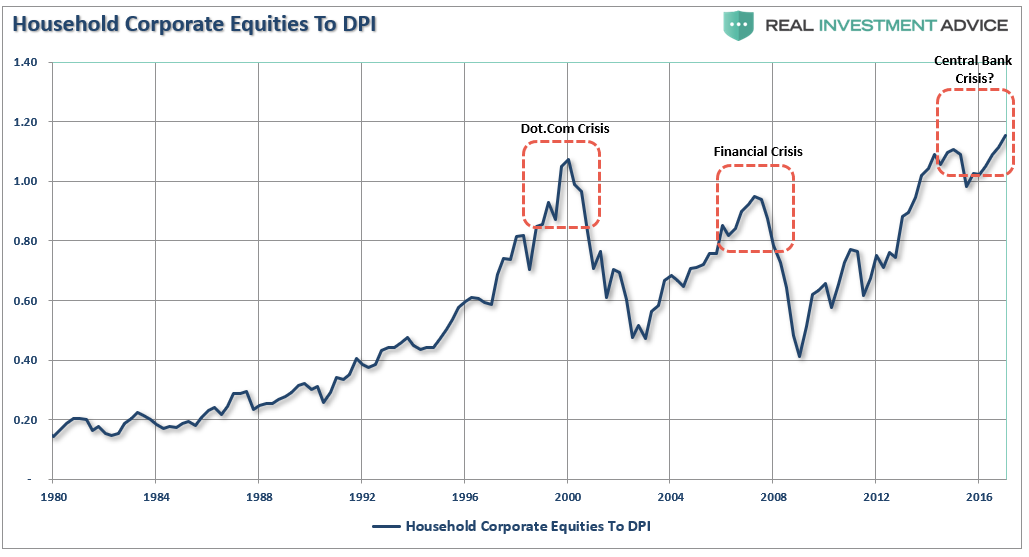

Ownership

Of course, the key ingredient is ownership. High valuations, bullish sentiment, and leverage are completely meaningless if there is no ownership of the underlying equities. The two charts below show both household and corporate levels of equity ownership relative to previous points in history.

Once again, we find rising levels of ownership are a good thing as long as prices are rising. As prices rise, individuals continue to increase ownership in appreciating assets which, in turn, increases the price of the assets being purchased.

Momentum

Another key ingredient to rising asset prices is momentum. As prices rice, demand for rising assets also rises which creates a further demand on a limited supply of assets increasing prices of those assets at a faster pace. Rising momentum is supportive of higher asset prices in the short-term.

The chart below shows the real price of the S&P 500 index versus its long-term bollinger-bands, valuations, relative-strength, and its deviation above the 3-year moving average. The red vertical lines show where the peaks in these measures were historically located.

The Formulation

Like dynamite, the individual ingredients are relatively harmless. However, when the ingredients are combined they become potentially dangerous.

Leverage + Valuations + Psychology + Ownership + Momentum = “Mean Reverting Event”

Importantly, in the short-term, this particular formula does indeed remain supportive for higher asset prices. Of course, the more prices rise, the more optimistic the investing becomes as it becomes common to believe “this time is different.”

While the combination of ingredients is indeed dangerous, they remain “inert” until exposed to the right catalyst.

These same ingredients were present during every crash throughout history.

All they needed was the right catalyst.

The catalyst, or rather the “match that lit the fuse,” was the same each time.

The Catalyst

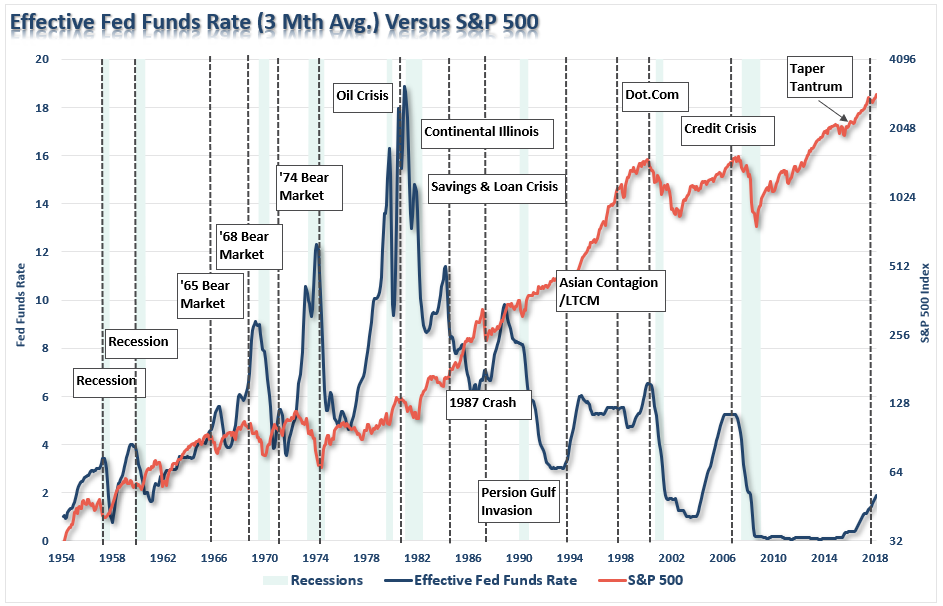

In the U.S., the Federal Reserve has been the catalyst behind every preceding financial event since they became “active,” monetarily policy-wise. As shown in the chart below, when the Fed has embarked upon a rate hiking campaign, bad “stuff” has historically followed.

With the Fed expected to hike rates 2-more times in 2018, and even further in 2019, it is likely the Fed has already “lit the fuse” on the next financially-related event.

Yes, the correction will begin as it has in the past, slowly, quietly, and many investors will presume it is simply another “buy the dip” opportunity.

Then suddenly, without reason, the increase in interest rates will trigger a credit-related event. The sell-off will gain traction, sentiment will reverse, and as prices decline the selling will accelerate.

Then a secondary explosion occurs as margin-calls are triggered. Once this occurs, a forced liquidation cycle begins. As assets are sold, prices decline as buyers simply disappear. As prices drop further, more margin calls are triggered requiring further liquidation. The liquidation cycle continues until margin is exhausted.

But the risk to investors is NOT just a market decline of 40-50%.

While such a decline, in and of itself, would devastate the already underfunded 80% of the population that is currently woefully under-prepared for retirement, it would also unleash a host of related collapses throughout the economy as a rush to liquidate holdings accelerates.

The real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely. The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping will cause a debacle of mass proportions. It will require a massive government bailout to resolve it.

But it doesn’t end there. Consumers are once again heavily leveraged with sub-prime auto loans, mortgages, and student debt. When the recession hits, the reduction in employment will further damage what remains of personal savings and consumption ability. The downturn will increase the strain on an already burdened government welfare system as an insufficient number of individuals paying into the scheme is being absorbed by a swelling pool of aging baby-boomers now forced to draw on it. Yes, more Government funding will be required to solve that problem as well.

As debts and deficits swell in coming years, the negative impact to economic growth will continue. At some point, there will be a realization of the real crisis. It isn’t a crash in the financial markets that is the real problem, but the ongoing structural shift in the economy that is depressing the living standards of the average American family. There has indeed been a redistribution of wealth in America since the turn of the century. Unfortunately, it has been in the wrong direction as the U.S. has created its own class of royalty and serfdom.

All the ingredients for the next market crash are currently present. All that is current missing is the “catalyst” which ignites it all.

There are many who currently believe “bear markets” and “crashes” are a relic of the past. Central banks globally now have the financial markets under their control and they will never allow another crash to occur. Maybe that is indeed the case. However, it is worth remembering that such beliefs were always present when, to quote Irving Fisher, “stocks are at a permanently high plateau.”