Protective Asset Strategies for Uncertain Stock Environments

Emerging volatility in stocks requires a strategic outlook from investors.

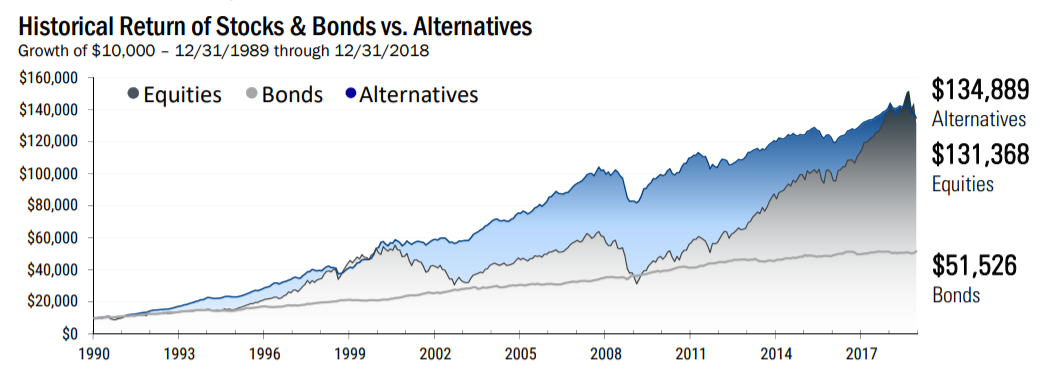

Increasingly uncertain market scenarios require innovative investment strategies capable of meeting challenges present in more dynamic market environments. But history has shown that traditional buy-and-hold equity/income strategies fail to adequately address these demands. Over the past 25 years, alternatives to stocks and bonds have consistently delivered higher returns, on lower volatility, during the period.

Balanced approaches to position volatility can significantly reduce the drawdowns investors typically face during protracted periods of market stress. One of the best examples of this comprehensive approach can be found in the Catalyst/Millburn Hedge Strategy Fund (MBXIX), a mutual fund which employs complementary active/passive investment strategies that consistently outperform traditional long-only equity investments.

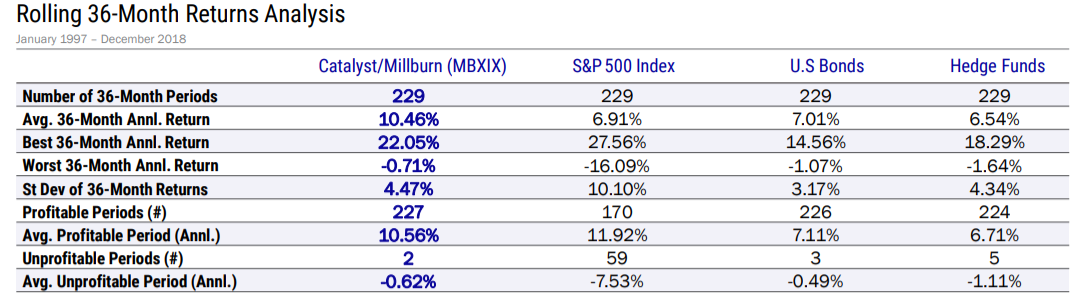

MBXIX operates as a globally-diversified portfolio of equity, interest rate, and currency instruments, in conjunction with futures contracts on commodities in the agricultural, metals and energy sectors. Negatively correlated during stress periods for equities, historical backtesting has demonstrated that this systematic, quantitative, multi-strategy design responds well to dynamic market conditions:

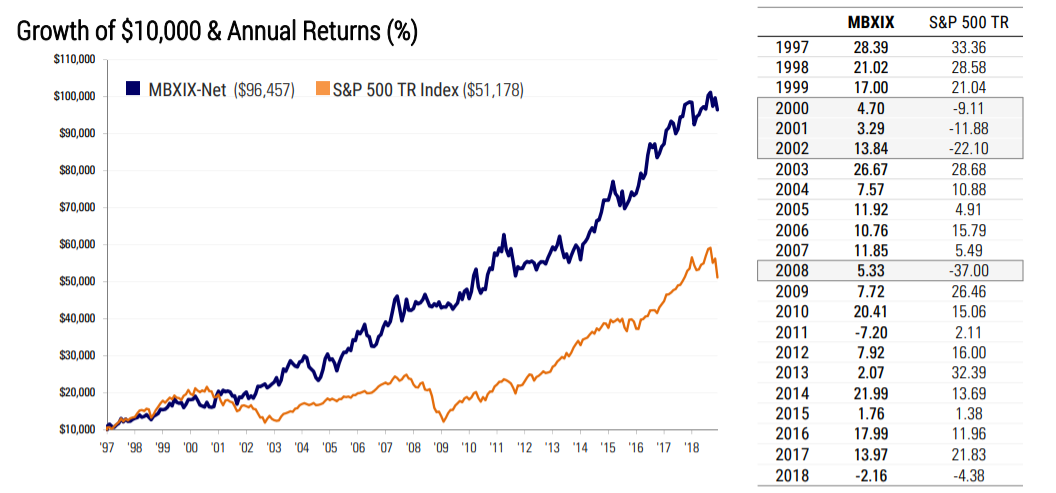

Since 1997, MBXIX has produced average annual returns of 10.85%. This comfortably surpasses the 7.7% average annual returns that are associated with the S&P 500 over the same period. In the 22 years since its inception, the Catalyst/Millburn Hedge Strategy Fund has experienced negative annual performances on only two occasions, and the fund generated positive returns for investors during critical stress years for equities.

Impressively, MBXIX was positive in 2000, 2001, 2002, and 2008 — even while the S&P 500 encountered substantial losses (-9.11%, -11.88%, -22.10%, and -37.00% respectively). These elevated long-term results confirm that the MBXIX blueprint, with its potential to invest in over 125 markets, has consistently protected its invested capital and worked as an effective shock-absorber during periods of rising price volatility.

MBXIX has a structural advantage over most long-only mutual funds because it combines managed futures positioning with a stabilizing equity strategy. The equity exposure component yields a portfolio of global/U.S. ETFs that is guided by a relatively passive buy-and-hold outlook. This approach typically performs best during calm markets, e.g., 2017, while managed futures tend to perform best in high-volatility environments which are frequently negative for equities, e.g., 2008.

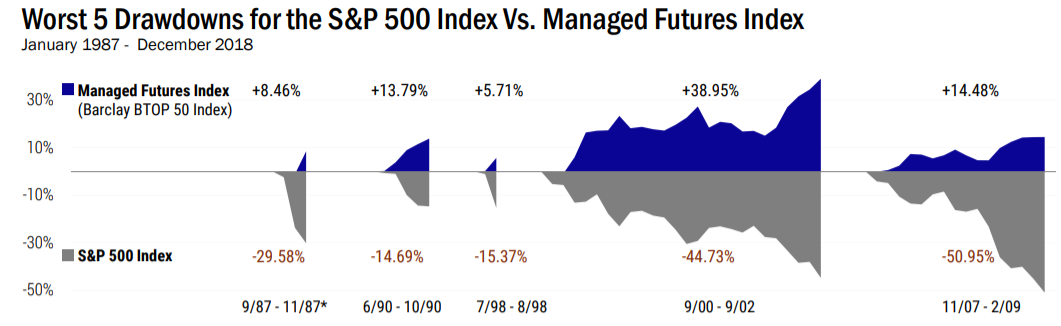

Asset correlation and risk analysis considerations define the fund’s goal of maximizing diversification. Long-term backtesting data show that this dynamic approach is capable of driving superior returns and protecting investors during shocks to global equity markets (including the worst S&P 500 drawdowns and quarters since 1987):

These performances show that diverse asset strategies enable investors to hedge risks and merge the strengths of each approach. For more than two decades, the portfolio designs of MBXIX have surpassed the total return from the S&P 500 by a wide margin (3.15%). At the same time, the fund has limited its maximum drawdowns to 22.11% (versus 50.95% for the S&P 500).

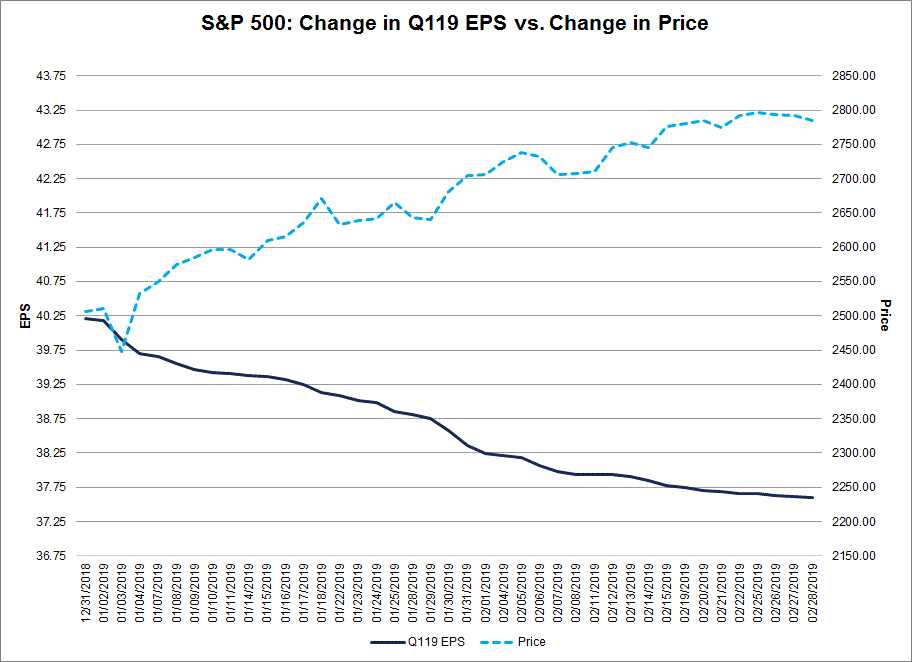

In December 2018, the CBoE Volatility Index (VIX) spiked to levels above 30, and evidence of continued economic uncertainty has created a precarious trading environment for stock investors. Those negative trends may have received additional confirmation in the form of a weaker consensus outlook for EPS in the first quarter of this year. Ultimately, this highlights a pressing need for active investment strategies that are capable of mitigating potential losses.

During the first two months of 2019, bottom-up EPS estimates for the S&P 500 were lowered from $40.21 to $37.60 (a decline of 6.5% for the first quarter period). This is 4.1% below the 5-year average and the single largest percentage reduction since the first quarter of 2016, when estimates were lowered by 8.4%. Even as the consensus outlook for earnings has deteriorated, however, market valuations have continued moving higher. The S&P 500 posted gains of 11.1% during the months of January and February, and the index is currently holding within striking distance of its all-time highs:

Expanding divergences between stock valuations and their underlying earnings fundamentals should trigger warning signals for investors. Downside revisions to Q1 2019 EPS estimates have been made for each of the 11 industry sectors in the S&P 500, with the most drastic reductions present in energy (32.3%), materials (15.2%) and technology (8.2%). Nine sectors in the S&P saw declines in the bottom-up EPS consensus that were larger than the 5-year historical average.

Recent inversions in the yield curve and expectations for weakness in Q1 earnings have coincided with sustained buying activity in gold and silver markets. In the end, this suggests that investors might be making an initial move toward safe-haven assets as a way of protecting against another round of volatility in stocks.

Ultimately, the Catalyst/Millburn Hedge Strategy Fund is an exceptional breed and rare find for safety-oriented investors. Clearly, the experienced management team understands that investors do not need another conventional mutual fund. As an innovative product that is constantly evolving, Millburn’s research is designed to carry investors through bull and bear markets while carefully considering risk and seeking to extract as much value as possible. The approach is constructed with characteristics that investors should consider when aiming for enhanced returns with lower correlation to the common indexes.

This article was contributed by Dividend Investments