Everyone loves a good turnaround story. Companies that fix poor corporate governance can unlock significant value and deliver market-beating returns to investors.

However, turnaround efforts also tend to involve significant one-time expenses – restructuring, divestitures, write-downs, etc. – that lead GAAP earnings to underestimate the improvement in a company’s profitability.

This firm has dramatically improved its profitability since adding return on invested capital (ROIC) to its executive compensation plan three years ago, but GAAP earnings have risen much slower. The company also has a cheap valuation and significant growth opportunities due to new energy efficiency regulations. Regal Beloit (RBC) is this week’s Long Idea.

GAAP Results Understate RBC’s True Profit Growth

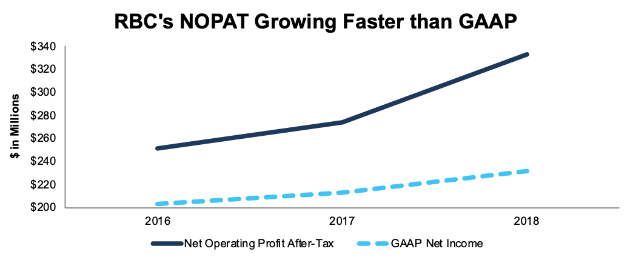

Investors who focus solely on reported GAAP net income get a misleading view of RBC’s profit growth. Over the past two years, RBC’s GAAP net income has risen by 7% compounded annually. On the other hand, after-tax operating profit (NOPAT) has risen by 15% compounded annually, per Figure 1.

Figure 1: RBC’s GAAP Net Income Vs. NOPAT Since 2016

Image Source: New Constructs, LLC

Sources: New Constructs, LLC and company filings

The disconnect can be attributed to the numerous accounting loopholes that make reported results a poor representation of a company’s true recurring profits. Specifically, we removed the following non-operating expenses from RBC’s GAAP net income in 2018:

- $20 million in increased LIFO reserves

- $17 million in costs related to the exit of its Hermetic Climate business

- $8 million in restructuring costs

In total, we identified $101 million (3% of revenue) in net non-operating expenses that must be removed from GAAP net income to calculate RBC’s true profits. After these adjustments, we found that 2018 NOPAT grew 21% year-over-year (YoY) while GAAP net income grew by just 9% YoY.

Focus on ROIC Spurs Turnaround

RBC operates in the electric motor and power transmission business. The company’s products power commercial and residential HVAC systems, industrial equipment, and a variety of appliances across many different sectors. The company competes based on the price, reliability, and energy efficiency of its products.

In the past, RBC utilized acquisitions as its primary strategy for growth. In 2014, the CEO even said they had a “bias towards acquisition.” From 2011-2015, the company completed over a dozen acquisitions worth over $2.5 billion (128% of its invested capital at the start of that period).

In theory, these acquisitions were supposed to improve the company’s competitive advantage through economies of scale and a wider variety of products. In reality, this strategy did not deliver the anticipated results. From 2011-2015, the company’s ROIC declined from 11% to 5%, and its stock declined by 15% while the S&P 500 was up 60%.

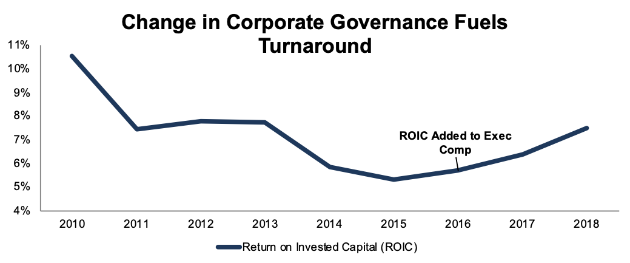

Faced with the failure of the acquisition-driven strategy, RBC’s leadership changed course in 2016. The company tied 50% of its long-term stock grants to ROIC and began selling off non-core business lines. Since the end of 2015, RBC has completed or initiated the divestiture of over $110 million (3% of invested capital) in non-core units. Figure 2 shows that this new focus on capital allocation (as opposed to “accretive acquisitions”) led to a significant improvement in ROIC.

Figure 2: RBC’s ROIC Since 2010

Image Source: New Constructs, LLC

Sources: New Constructs, LLC and company filings

Cutting back on acquisitions and divesting non-core businesses allows RBC to focus on its core competencies. In recent years, the company has scaled back its manufacturing footprint, invested in automation to reduce costs, and debuted innovative new products to benefit from growing trends in electrification and energy efficiency.

Innovation Creates Competitive Advantage

In particular, RBC has focused its efforts on two major innovations in recent years that should give it a significant advantage over its peers, especially in the residential and commercial HVAC space. Those innovations are:

Axial Motors: In the past, almost all HVAC systems were powered by radial motors, which are bulky and heavy. The size and weight of these motors placed significant restrictions on the design of large HVAC systems.

In 2016, RBC debuted a new type of electric motor for HVAC systems – the Axial Integral Horsepower Motor. Axial motors are smaller, more easily configurable, and more energy efficient than radial motors. The success of the company’s new axial motor products have helped drive solid organic growth in its commercial HVAC business. The company does not break out the exact size of its commercial HVAC business, but it is the largest portion of its Commercial & Industrial Systems segments, which accounts for 47% of revenue.

RBC continues to innovate in this area and is currently partnering with the Department of Energy and Texas A&Mto drive further gains in energy efficiency.

Internet of Things: RBC’s other main focus for its innovation efforts has been on connectivity and the Internet of Things (IoT). Connected motors make it easier to diagnose and fix problems, perform preventative maintenance, and optimize energy efficiency.

RBC’s innovations in the IoT area were recently validated when its Genteq Ensite motor won an innovation award at the 2019 AHR Expo, the largest HVAC convention in the world.

Not only is the Ensite motor a recognized leader in the IoT space, it also complies with soon-to-be effective energy efficiency regulations for residential furnace fans. These two factors should help this product quickly gain traction and market share and provide a boost to the company’s Climate Solutions segment, which accounts for 30% of revenue.

New Regulations Provide Opportunity

The Department of Energy’s Fan Energy Rating (FER), which sets higher energy efficiency standards for residential furnace fans, will go into effect in July of this year. According to industry insiders, the new regulations will practically require all new furnace fans to be powered by electronically commutated motors (ECMs), rather than the cheaper but less efficient standard induction motors.

This new regulation should lead to a shift to higher-priced products for RBC, and opportunities for it to gain market share with new products like the Ensite motor. RBC has long-term relationships with most of its major HVAC customers, which positions it as a trusted supplier for companies that need to comply with new regulations.

Currently, the company projects the implementation of FER to add $40 million in incremental revenue (1% of 2018 revenue). Similar regulations around walk-in coolers and freezers and pool pumps are slated to go into effect in 2020 and 2021 and should have a similar effect of shifting demand towards ECMs.

Figure 3 shows how significant a shift to higher-priced, higher-margin motors would be for RBC, which earned nearly half of its $3.4 billion in revenue in 2018 from small motors.

Figure 3: RBC’s Revenue Breakdown by Product

Image Source: New Constructs, LLC

Sources: Regal Beloit Investor Relations

Regulation and innovation-driven growth in the small motors business should more than make up for loss of revenue in other areas as RBC sells off more of its non-core businesses.

Tariffs/Trade Concerns Can Be Overcome

While tariffs are a real concern for RBC, recent changes to the business leave it better equipped to react to tariffs and maintain strong margins.

Consolidation of its global manufacturing footprint has been an important factor for RBC in both cutting costs and improving flexibility. From 2013-2018, RBC decreased its global footprint from ~10 million square feet to under 8 million square feet. This reduction includes a decrease in its China footprint from 2.2 million square feet to 1.5 million.

As part of RBC’s consolidation efforts, it has worked on making it easier to transfer production between facilities. Even though ~20% of its manufacturing footprint remains in China, the company has the ability to transfer production outside the country for tariff-sensitive goods.

For situations when tariff avoidance is impossible, RBC’s profit-improving innovations give it greater ability to absorb these additional costs. On its most recent earnings call, management specifically singled out price increases as a way to respond to tariffs and said the firm implemented a large number of price increases across all segments in the second half of 2018.

RBC’s consistent margins further prove its ability to respond to tariffs. From 2015-2018, gross margins have stayed consistent at 26-27%.

Improving ROIC Correlated with Creating Shareholder Value

Numerous case studies show that getting ROIC right is an important part of making smart investments. Ernst & Young recently published a white paper that proves the material superiority of our forensic accounting research and measure of ROIC. The technology that enables this research is featured by Harvard Business School.

Per Figure 4, ROIC explains 74% of the difference in valuation for the peers listed in RBC’s 2018 proxy statement. RBC’s stock trades at a discount to peers as shown by its position below the trend line.

Figure 4: ROIC Explains 74% Of Valuation for RBC Peers

Image Source: New Constructs, LLC

Sources: New Constructs, LLC and company filings

If the stock were to trade at parity with its peer group, it would be worth $129/share – a 68% upside to the current stock price. Given the firm’s rising profits and significant growth opportunities, one would think the stock would garner a premium valuation. Below we’ll use our DCF model to quantify just how high shares could rise assuming conservative profit growth.

RBC Is Priced for Limited Profit Growth

Despite its strong fundamentals, RBC remains cheap by both traditional and advanced valuation metrics. At its current price of $77/share, RBC has a P/E ratio of 16 and P/B of 1.6, which is below the S&P 500 average of 22 and 2.8.

When we analyze the cash flow expectations baked into the stock price, we also see that RBC is significantly undervalued. At $77/share, RBC has a price to economic book value (PEBV) of 1.2. This ratio means the market expects RBC to grow NOPAT by no more than 20% for the remainder of its corporate life. Such expectations seem overly pessimistic for a company that grew NOPAT by more than 20% last year alone.

If we assume that RBC can maintain 2018 NOPAT margins (9%) and grow NOPAT by 6% compounded annually – in line with HVAC industry projections – over the next decade, the stock is worth $127/share today – a 65% upside. See the math behind this dynamic DCF scenario.

Sustainable Competitive Advantages That Will Drive Shareholder Value Creation

Here’s a summary of why we think the moat around Regal Beloit’s business will enable the company to generate higher profits than the current valuation of the stock implies. These competitive advantages help prevent competition from taking market share by offering better products/services at a lower price.

- Innovation in energy efficiency and the Internet of Things

- Flexible, low cost manufacturing capabilities

- Long-term relationships with major customers

What Noise Traders Miss with RBC

These days, fewer investors focus on finding quality capital allocators with shareholder friendly corporate governance. Instead, due to the proliferation of noise traders, the focus leans toward technical trading while high-quality fundamental research is overlooked. Here’s a quick summary for noise traders when analyzing RBC:

- NOPAT rising faster than GAAP net income

- Change in executive compensation

- Reduced exposure to Chinese manufacturing

Faster Than Expected Growth Could Push Shares Higher

RBC currently projects organic growth in the low-to-mid single digits for 2019. However, the implementation of FER and the growing adoption of axial motors presents the opportunity to surprise to the upside. If RBC’s new products gain market share at a faster rate than expected, they could deliver solid earnings surprises to investors.

More product announcements could also provide a boost to shares. RBC’s collaboration with the Department of Energy is slated to conclude this year, and if they announce a significant improvement in energy efficiency that should send shares higher.

Longer-term, we expect improved cash flow from superior capital allocation to provide a boost to shares. As the company sells off underperforming assets and forgoes wasteful acquisitions, it frees up more capital to invest in innovation or return to shareholders.

Dividends and Share Repurchase Offer 4.8% Yield

RBC has increased its quarterly dividend in 14 consecutive years. The current dividend of $0.28/share provides an annualized 1.3% yield. Best of all, RBC generates the necessary cash flow to continue paying its dividend. Over the past three years, RBC has generated $900 million (25% of market cap) in free cash flow while paying about $130 million in dividends.

In addition to dividends, RBC returns capital to shareholders through share repurchases. In 2018, RBC repurchased $123 million (3.4% of market cap) worth of shares. The company currently has $197 million remaining on its repurchase authorization.

Insider Trading and Short Activity are Minimal

Insider activity has been minimal over the past 12 months, with 70 thousand shares purchased and 192 thousand shares sold for a net effect of 122 thousand shares sold. These sales represent less than 1% of shares outstanding.

There are currently 564 thousand shares sold short, which equates to 1% of shares outstanding and 2.5 days to cover. There seems to be little appetite in the market to bet against this stock.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst[1] findings in Regal Beloit’s fiscal 2018 10-K:

Income Statement: we made $160 million of adjustments, with a net effect of removing $101 million in non-operating expense (3% of revenue). We removed $29 million in non-operating income and $131 million in non-operating expenses. You can see all the adjustments made to RBC’s income statement here.

Balance Sheet: we made $984 million of adjustments to calculate invested capital with a net increase of $486 billion. The most notable adjustment was $278 million in asset write-downs. This adjustment represented 7% of reported net assets. You can see all the adjustments made to RBC’s balance sheet here.

Valuation: we made $1.8 billion of adjustments with a net effect of decreasing shareholder value by $1.5 billion. You can see all the adjustments made to RBC’s valuation here.

Attractive Funds That Hold RBC

The following funds receive our Attractive-or-better rating and allocate significantly to Regal Beloit.

- Meritage Value Equity Fund (MVEBX) – 2.6% allocation and Attractive rating.

- Fidelity Environment and Alternative Energy Portfolio (FSLEX) – 2.4% allocation and Attractive rating.

- SPDR MFS Systematic Value Equity ETF (SYV) – 2.0% allocation and Very Attractive rating.

This article originally published on April 24, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.