Source: Streetwise Reports 07/26/2018

The U.S. Department of Commerce investigation into whether uranium imports threaten national security could lead to the imposition of tariffs that would benefit firms with American mines such as Azarga Uranium. Streetwise Reports spoke with Azarga’s chairman Glenn Catchpole and CEO Blake Steele about the state of the uranium market and the company’s recent merger with URZ Energy.

The Energy Report: In response to a Section 232 petition by Energy Fuels Inc. (EFR:TSX; UUUU:NYSE.American) and Ur-Energy Inc. (URG:NYSE.MKT; URE:TSX), the U.S. Commerce Department declared that it has opened an investigation into whether uranium imports threaten U.S. national security. How does this change the market landscape for uranium?

Blake Steele: This is potentially a very exciting catalyst for the U.S. uranium industry. President Trump has been protective of other U.S. industries, imposing steel and aluminum tariffs on the back of a Section 232 petition as well. And currently, the U.S. produces less than 5% of its annual uranium consumption while nuclear energy accounts for approximately 20% of the electrical grid.

Ultimately, this investigation has the potential to create a uranium market with two prices. One, there’s going to be a global price for production destined for non-U.S. consumption. And two, there’s going to be a price for U.S. domestic production, which will likely be meaningfully higher. Azarga Uranium Corp.’s (AZZ:TSX) asset suite is well positioned to take advantage of this.

In terms of timing, the Secretary of Commerce has 270 days to report and propose recommendations to President Trump. Trump then has 90 days to take action on those recommendations, should any actions be necessary to address the threat.

TER: Aside from this investigation, what other things are happening on a macroeconomic level with uranium? Prices have been low for a long time.

BS: You’re right, prices have been depressed for a prolonged period of time. Globally, we’re finally starting to see producers slashing supply. Producers have eliminated or are in the process of eliminating more than 30 million pounds (30 Mlb) of annual production since 2016. In conjunction, utilities have been underbuying in recent years, running down stockpiles and contract positions put in place pre-Fukushima, when European and U.S. utilities were concerned about market tightness due to rapid growth out of China.

You couple this with large funds being established to hold physical uranium, the U.S. Department of Energy halting sales to fund clean-up programs and Cameco Corp. (CCO:TSX; CCJ:NYSE) buying large volumes in the spot price while Japan continues to restart reactors, it’s a bit of a perfect storm here. All of these events are putting pressure on prices as spot supply begins to dry up.

In conjunction again with this, demand is growing. China is forecast to construct six to eight nuclear reactors per year, increasing to 10 after 2020. Japan will require approximately 30 reactors being back online to achieve its goal of powering 20?22% of its grid through nuclear.

One of the most significant upcoming catalysts could be McArthur River going into care and maintenance beyond the previously announced 10-month suspension. I would expect to see an announcement on this before the end of this quarter. (Editor’s note: On July 25, Cameco announced the suspension of McArthur River for an indeterminate duration.)

So all of these factors considered, I think it’s presenting a very interesting dynamic for the next 12 months in the uranium sector, the start of potentially a bull market here.

TER: One thing that I’m curious about is that most of the utilities that require uranium buy it on long-term contracts, and those contracts in the past have been in the $50 per pound ($50/lb) range. The spot price is well below that. As those contracts expire are the utility operators buying on the spot market? Are they going for new long-term contracts at lower rates?

BS: Contracting to date has been generally slow. Utilities over the last few years have been picking up pounds on the spot market, but this fundamentally has to change. As a result of those factors previously mentioned, the supply in the spot market is really drying up. Now, couple that with the fact that in excess of 75% of producers are not making money at current spot prices, they’re not going to be entering into contracts with utilities at anywhere near this price point. So I think when the utilities start contracting in a meaningful way, we are going to see long-term prices substantially north of where they and the spot price are today.

TER: Let’s turn now to your merger. Azarga completed the merger with URZ Energy Corp. on July 5. Would you talk a little bit about the merger and the benefits of the amalgamation?

BS: From our perspective, the merger presented an opportunity to create the only pure-play in situ recovery (ISR)-focused uranium developer in the U.S. The merged company has in excess of 30 Mlb of Measured and Indicated resources and 8.7 Mlb of Inferred resources located in the U.S. So we’re talking about scale focused in the U.S., which, with this 232 petition, seems to be the place you want to be right now.

The company’s flagship asset, the Dewey Burdock project in South Dakota, is the highest-grade undeveloped ISR project in the U.S. And adding URZ’s pipeline of assets, which includes the Gas Hills project in Wyoming, was a natural fit.

The merger also created a vehicle with an enhanced market position and a more diversified shareholder base, broadening investor and analyst appeal. Creating additional liquidity and investor interest in the uranium sector I think is an important goal for any vehicle.

TER: How have you consolidated the management teams?

BS: The combined management team is very interesting. We have over 100 years of experience in the ISR space, including development, design, permitting and operational experience. We have a very strong board with a diverse skill set, led by Glenn Catchpole as our chairman. Glenn had great success building and ultimately selling Uranerz Energy Corp. in the past. Our chief operating officer, John Mays, has 20 years of experience in the design, construction and operation of ISR mines in both the U.S. and Kazakhstan. All in all, I’d say we have a very strong management team poised to advance our asset suite and continue to unlock value for our shareholders. From my perspective, working with Glenn provides me with the opportunity to leverage Glenn’s vast expertise and experience. And ultimately, together, the combined management team has a larger network that will provide more opportunities for Azarga and our shareholders.

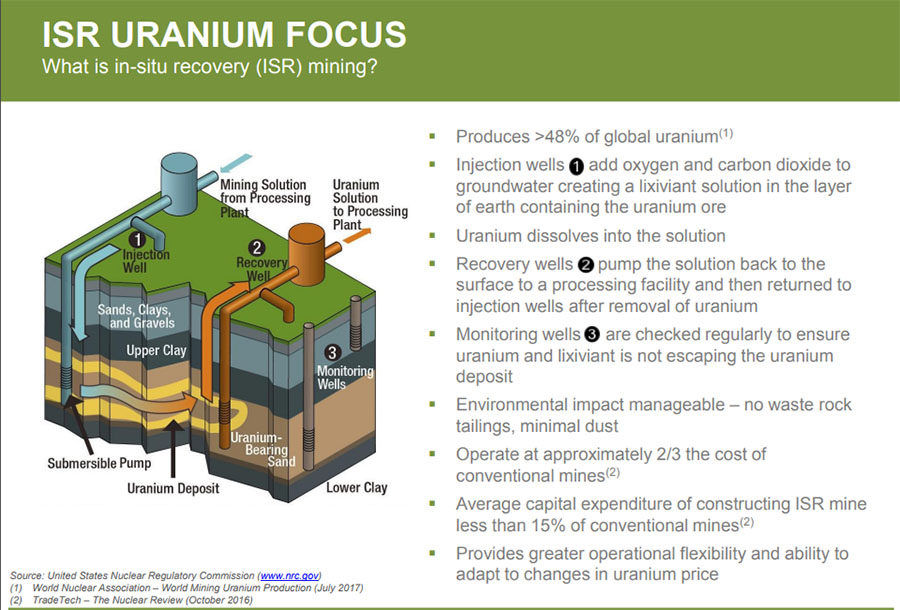

TER: You mentioned that Azarga has one of the largest portfolios of in situ recovery uranium projects in the U.S. Can we talk about ISR for a moment? Does it provide advantages over conventional mining?

Glenn Catchpole: Yes. In the U.S. our deposits typically are not high grade when you compare them to, say, the Athabasca Basin. But our advantage is that in the U.S. we do have deposits that can be produced at competitive levels using the ISR technology.

To give you an example, in the early 1980s, when the uranium industry all over the world went bust, prices went down to less than $10/lb and essentially all the conventional uranium mines in production in the U.S. at that time could not compete with the high-grade deposits in, as I said, the Athabasca Basin deposits in Canada. The only ones that were left in production in the U.S. were the ISR mines that we had in places like Texas, Wyoming and Nebraska.

Those ISR mines were able to still make a return on their investment that was acceptable from a business standpoint. That’s because the technique doesn’t require excavating big pits, and doesn’t require sinking shafts. In ISR mining, we don’t have those considerable expenses.

Another important aspect is from a permitting and regulatory standpoint; we do not need tailings ponds, as tailings ponds require considerable reclamation at the conclusion of mining. So this makes us cost competitive with other places in the world. And we see that trend continuing, as noted by production out of Kazakhstan on the Inkai project that I worked on, where they’re able to compete as probably the lowest cost or next to lowest cost producer in the world and, again, using the ISR technology.

BS: Glenn hit the nail on the head there. Another thing that’s important to point out is that approximately 50% of today’s uranium is produced using the ISR mining method. So it’s not a new methodology. It’s existed for decades. It’s widely utilized.

ISR projects also provide greater operational flexibility and provide the company with the ability to adapt to changing uranium prices. Projects can ramp up and be built in a matter of months, as opposed to 5 or 10 years like conventional assets in the basin, with significantly less upfront capex, which ensures that projects in the advanced permitting stage, such as our Dewey Burdock, are well positioned to take advantage of the next uranium bull market. So I think having the U.S.’s highest-grade undeveloped ISR project, Dewey Burdock, really helps set us apart from our peers.

TER: Speaking of Dewey Burdock, Azarga’s flagship project in South Dakota, would you bring us up to date on it and where the permitting situation is right now?

BS: Dewey Burdock is the highest-grade undeveloped ISR uranium project in the U.S. The project has forecast first quartile C1 cash costs and only requires $27 million of capex to achieve initial production. Life-of-mine production is expected to be 9.7 Mlb U3O8 with annual steady state production of 1 Mlb.

We are also very excited about the growth potential of the Dewey Burdock resource. We are currently working on a resource update using newly identified mineralization, which will nearly double the number of mineralized intercepts at Dewey Burdock. The additional mineralization is contiguous with existing ISR resources at Dewey Burdock and falls within the existing Nuclear Regulatory Commission license (NRC) boundaries. On the back of this, we are aiming to announce a resource update later this quarter followed by an updated preliminary economic assessment (PEA) in Q4/18 or early Q1/19 in which we expect improved project economics due to the increased scale of the project.

On the permitting front specifically, we are working toward finalizing the permitting process. We have received the NRC license as well as the draft Environmental Protection Agency permits. And the state permits have been recommended for approval. There is one remaining contention being worked through on the NRC license, but we expect that to be resolved sooner rather than later.

TER: Dewey Terrace has the possibility of becoming a satellite operation. What is its status?

BS: We have identified 259 mineralized drill holes at Dewey Terrace, which is directly adjacent to Dewey Burdock but on the Wyoming side of the border. Dewey Terrace could be a potential satellite project to Dewey Burdock, and we are continuing to review project information with the goal of identifying a uranium resource here. So for us, Dewey Terrace is yet another catalyst that we can potentially leverage in the next 12 months.

TER: Does the fact that it’s located in a different state complicate matters?

BS: Glenn has developed, permitted and designed the Nichols Ranch project in Wyoming with Uranerz. So we don’t foresee that being an issue, just really part of the process in the future.

TER: Let’s go on to the Gas Hills project, which belonged to URZ Energy. Is it the next project that you anticipate being developed? What is its status?

BS: The Gas Hills District is a prolific uranium district. Approximately 100 Mlb of uranium were mined here from the 1950s to the late 1980s. We are currently evaluating how ISR mining may positively impact future development options at the Gas Hills project. Historically, the majority of mining in this area was done via open-pit mines, and it wasn’t necessarily considered from an ISR perspective. To date, three of the five deposits at Gas Hills have been shown to be amenable to ISR mining, and we are very excited about the ISR prospects. So the key here for us is to focus on the ISR potential of the project and to move the project forward to fill our development pipeline.

GC: We’ve been doing some studies that indicate to me that considerable pounds could be mined from Gas Hills using the in situ leach technology. It wasn’t used out there in the past just because historically mining was conventional mining. But once the price went south, as I mentioned earlier, those Gas Hills mines all shut down from the conventional mining. And there are still considerable pounds out there, and the majority of those pounds, I feel, are extractable by ISR. So I’m very optimistic how that can fit into our overall planning, and of course, a lot of that planning and decision-making will hinge on what happens to the price of uranium going forward.

TER: Let’s talk about Azarga’s share structure post merger. How many shares are outstanding? What percentage is closely held?

BS: We have approximately 156 million shares outstanding. I would say about 40% of the register is closely held. Management, directors and founders have a lot of skin in the game, and we are certainly aligned with our shareholders when it comes to this. I think it’s always important. You want to make sure that management is always aligned with your shareholders.

TER: Do you have funding in hand to take Dewey Burdock to production?

BS: We will need to secure project financing to develop the project. The initial capex is only $27 million. Our plan of attack here would be to have a funding solution in place prior to or concurrent with the finalization of the permitting process for Dewey Burdock.

TER: Any parting thoughts?

BS: The next 12 months look very exciting for the sector and specifically our business. We’ve touched on a number of catalysts already?the resource update and the PEA update at Dewey Burdock, the permitting progression at Dewey Burdock, the satellite deposit in Dewey Terrace, as well as the continued evaluation of ISR development options at Gas Hills. All things considered, it’s a very exciting time for our business.

TER: Thanks for your time, Blake and Glenn.

Blake Steele is the president and CEO of Azarga Uranium. He joined the company in October 2014 as the chief financial officer and subsequently took on the roles of president and CEO. Prior to serving as the CFO of Azarga Resources, which merged with Powertech Uranium to form Azarga Uranium, Steele served as director of finance at SouthGobi Resources (part of the Ivanhoe Mines Group), and prior to that as manager, corporate development. Steele began his career with Deloitte & Touche, where he worked in both the audit and financial advisory practices. Steele graduated from the University of British Columbia with a Bachelor of Commerce degree. He is a Chartered Accountant and Chartered Business Valuator in Canada.

Glenn Catchpole is the chairman of Azarga Uranium. He served as a member of the Board of Directors and the CEO of Uranerz Energy Corp. from 2005 until 2015 when the company was sold to Energy Fuels Inc. for more than $150 million, creating the largest integrated uranium producer in the United States. Catchpole is a licensed engineer who holds an M.S. in civil engineering from Colorado State University. He has been active in the uranium solution mining industry since 1978, holding various positions including wellfield engineer, project manager, general manager and managing director of several uranium solution mining operations. He served as general manager and managing director of the Inkai uranium mine in the Republic of Kazakhstan, taking it from acquisition through feasibility study, joint venture formulation, government licensing, environmental permitting, design, construction and the first phase start-up.

Want to read more Energy Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None.

2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: Azarga Uranium and Energy Fuels. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Blake Steele and Glenn Catchpole had final approval of the content and are wholly responsible for the validity of the statements. Opinions expressed are the opinions of interviewees and not of Streetwise Reports or its officers.

4) Blake Steele: I was not paid by Streetwise Reports to participate in this management interview. I had the opportunity to review this for accuracy and am responsible for the content. I or my family own shares of the following companies mentioned in this discussion: Azarga Uranium.

5) Glenn Catchpole: I was not paid by Streetwise Reports to participate in this management interview. I had the opportunity to review this for accuracy and am responsible for the content. I or my family own shares of the following companies mentioned in this discussion: Azarga Uranium, Cameco and Energy Fuels.

6) Discussions are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

7) The discussion does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This discussion is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

8) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Azarga Uranium, a company mentioned in this article.

( Companies Mentioned: AZZ:TSX,

)