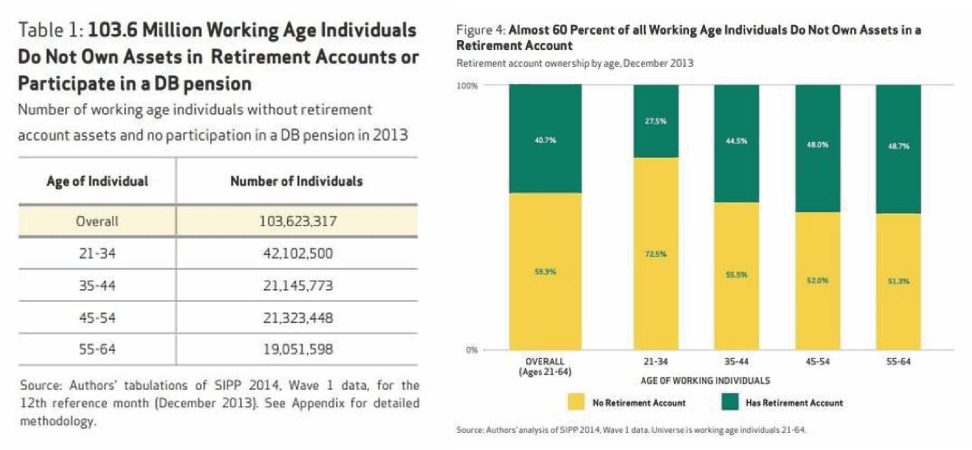

“Those fears are substantiated even further by a new report from the non-profit National Institute on Retirement Security which found that nearly 60% of all working-age Americans do not own assets in a retirement account.”

Here are some additional findings from the report:

Here are some additional findings from the report: