“Behold the turtle. He makes progress only when he sticks his neck out.” — James Bryant Conant

If you are planning for retirement, you have probably felt the pressures involved when looking at all of the different places to park your money. The financial landscape can be a complicated place, and the task of choosing between asset classes can seem daunting during the early stages of the process. Two of the most popular asset classes are stocks and bonds, and many newer investors often wonder which is best for a long-term retirement portfolio.

In any retirement portfolio, investors must understand the concept of market risk as it relates to their positions. This essentially refers to the possibility of losses relative to the potential for reward (gains) in the investment. These factors work hand-in-hand, but a seasoned financial advisor can help understand the nuances which are present when planning for retirement. We sat down with Adam Anderson, CEO of MRA Capital Partners to identify new strategies to turn the odds into our favor on the path toward building wealth. Below, we can find some tips we uncovered along the way.

Measuring Potential Returns

As a general rule, greater potential for gain tends to be associated with larger levels of risk. These factors can be understood when comparing the historical returns generated by investments in both stocks and bonds. When a retirement portfolio is designed by an industry expert and assets are properly allocated, risk is generally a short-term phenomenon. The potential for returns differs when we are comparing the advantages of stocks and bonds, and the appropriate selections for your retirement portfolio will depend heavily on your individual goals and needs.

Over the last century, U.S. Treasury Bills have acted as a proxy for money market accounts (generating yields of roughly 3.7% annually). Longer-term government bonds returns about 5.7% over the same period. Put in simple terms, if you invested $1 in long-term bonds in 1926 your investment would be worth about $100 in 2008. Stock investments, on the other hand, would have produced very different results (generating annual returns of 9.6% during these same periods). In this case, a $1 investment in large-cap stocks in 1926 would be worth about $2,000 just prior to the financial turmoil of 2008.

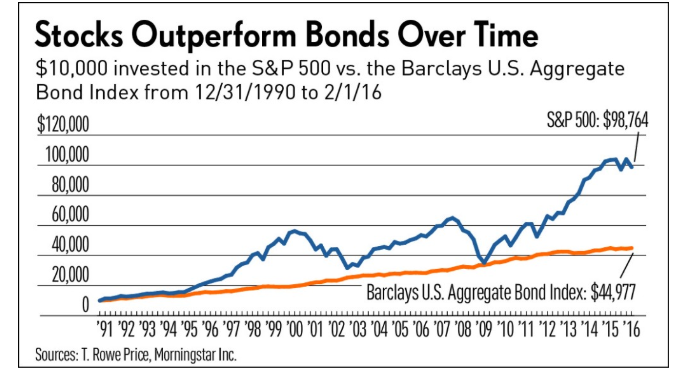

In the chart above, we can see the more recent trends in stock markets as they relate to the bond markets. Interestingly, there are some cases where the traditional correlations to not match the current tendencies. These asset classes have had periods characterized by similar returns (both small and large). This is precisely why retirement investors will consult an experienced financial advisor, so that it is easier to spot the differences in any given market climate.

“As a CFP and Financial Planner, I’ve practiced the principles of asset allocation and diversification through both bull and bear market cycles as well as expansion, contraction, and recessionary economic climates. Diversification between asset classes is paramount to a successful investment strategy,” Mr. Anderson explained.

“At the most broad level, the mix between stocks and bonds is most commonly debated especially among retail investors and their advisors. In my opinion, the most heavily overlooked asset class for individual investors are alternatives. Alternatives can be commodities, futures, real estate, private equity, art and other non stock or bond investments. Alternatives should make up between 10%-20% of a well diversified portfolio for the average investor but is much higher for some institutional investors, endowments, pensions and high net worth individuals. While I don’t personally endorse this, some even choose to invest only in non market based alternatives ignoring stocks and bonds completely,” Mr. Anderson explained.

“The benefit to alternatives is that when managed correctly, they should be non-correlated to stocks or bonds. Private equity and Real Estate tend to do a very good job at this. The challenge is finding the right managers and strategies that fit the investors goals and comfort level. Another challenge is investment minimums are generally very high and transparency is generally low when investing directly in real estate for example,” Mr. Anderson explained.

Limiting Risk in Retirement Portfolios

More broadly, stock markets have generated much higher average returns, and this is why retirement portfolios tend to be more heavily-centered in these areas. Of course, this added potential for return comes with added risk for the investment. But since the stock market tends to post positive results during the vast majority of market scenarios, any losses tend to be removed over time.

These are all risks which must be understood but when we have a well-constructed investment portfolio it becomes possible to turn the odds in our favor. Markets will always experience -boom-and-bust type periods in the broader economic cycle. But when a retirement portfolio is well-constructed and diversified, these risks can be mitigated and substantially reduced. Stock markets move higher during the vast majority of the time, and this is why buy-and-hold strategies tend to work best in generating returns and investment income.

“Heading into 2019, it’s no secret we are in the later stages of the current economic expansion and the federal reserve has made it very clear they plan to continue on their current path of raising rates. This along with the uncertainty surrounding the current political and trade headline risk is likely to continue to cause volatility in the stock and bond markets,” Mr. Anderson explained.

“If rates rise more rapidly than anticipated, bonds may prove to be less of a safe haven or diversifier than investors expected. Additionally, as the world economy continues to become more integrated, many of the more liquid asset classes like stocks, bonds, REITS, and even liquid alternatives like those access via ETFS or Mutual Fund may prove to be more correlated to each other then they have been in the past. In my opinion, carefully selected privately held investments are the best way to gain non-correlated exposure,” Mr. Anderson explained.

Understanding Time Horizons

Time is another important factor in any investment. Will you be retiring 10 years from now? Twenty years? Maybe much sooner? It is never too late to start planning your retirement portfolio. But the time you have until you stop working your regular job can be an important factor in determining which types of assets to include in your investment portfolio. If you have an extend time period before your retirement, there is often better opportunity for capital growth through stock investments. Conversely, if you are looking for short-term stability and income, bonds may offer advantages given your individual needs.

“There are risks associated with all investments. At MRA Capital Partners, we focus on privately held investments back by the hard asset of real estate. While these types of private equity and debt investments are not immune recessions, rising rates and other market forces, they very rarely behave like traditional stocks or bonds which may be a great complement to a balanced portfolio. Additionally, investments offered by MRA Capital Partners have a strong income component, many distributing 10% or more annually which make them a great complement or even alternative to bonds,” Mr. Anderson explained.

Of course, these are all factors which should be discussed with your investment advisor, and the answers will differ depending on your individual needs and goals. There is no substitute for individual attention and it must always be understood that “patience pays” in any financial markets investment. As the sage wisdom of James Bryant Conant tells us “Behold the turtle. He makes progress only when he sticks his neck out.” This suggests a certain level of risk can be taken, as long as those risks are measured and characterized by patience that is well-researched in the current market environment.

For this article, we interviewed Adam Anderson, CFP®, CRPC® CEO – Managing Partner of MRA Capital Partners.

This contribution originally appeared on PRO STOCK MARKETS, where we learn to trade with the pros.