Economic Data and Geopolitical Trends Indicate Continued Risk-Aversion in Markets

Image Source: Pixabay

Economic Data and Geopolitical Trends Indicate Continued Risk-Aversion in Markets

Geopolitical tensions dominated the narrative once again this week, as investors look to macro factors for the next directional cues. Earnings season continues in the U.S. market, and tech stocks experienced some increased buying activity toward the end of the week. Both the NASDAQ and the Dow Jones Industrial Average have posted gains for seven consecutive sessions, while the yield on the 10-year Treasury note finished the Friday session at 2.63%. Small gains were also visible in WTI crude oil, which has moved to $52.72/bbl in a continuation of the rebound in commodities which started in December 2018.

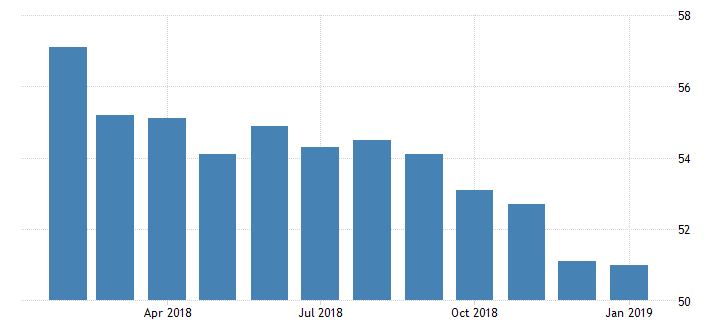

Forex markets have witnessed some interesting developments, as macroeconomic data out of Europe indicate the possibility of growing weaknesses in the region’s business sector. To start 2019, the long-term slowdown in manufacturing has led to the lowest services sector growth rates since the middle of 2013. In addition to this, broader demand levels have dropped to their lowest levels in four years. According to economic data and trading news feeds from AskTraders, the IHS Markit Eurozone Composite Final Purchasing Managers Index dropped from 51.1 in November to 51.0 in December. This indicator broadly measures economic health in the region and this is now the lowest print that we have seen since the month of July in 2013.

Of course, any economic reading over 50 is indicative of expansion in Europe but the trends here are clearly pointed in the downward direction and there is now growing risk that the region will fall into contractionary territory at some point this year.

(PMI Chart Source: Trading Economics)

Comments from the chief business economist from IHS Markit suggest that these declines in PMI have created GDP projections of 0.1% for the eurozone in the first quarter of 2019. This is a significant decline from the prior quarterly GDP estimates of 0.4% which were visible last month. These reports generated sizable weakness in the EUR/USD forex pair, which continues to pressure the downside within its long-term descending triangle formation.

(Forex Price Data: AskTraders.com)

Further moves in the currency markets were propelled by unresolved issues related to global trade talks between the U.S. and China. Trending moves in the U.S. dollar were influenced in the opposite direction after news reports which indicated that Chinese President Xi Jinping and U.S. President Donald Trump will not be meeting prior to the upcoming trade deal deadline (which is currently in place for March 2, 2019).

(Forex Price Data: AskTraders.com)

The leadership bodies in the U.S. and China have not necessarily ruled out a meeting to discuss various options, but these latest developments suggest that prior deadlines will not be met and this has led to periods of risk aversion which have benefited traders with short positions in the USD/JPY. The forex pair is trading near the bottom of its symmetrical triangle formation and this could produce further losses in the USD/JPY if support levels are broken to the downside.

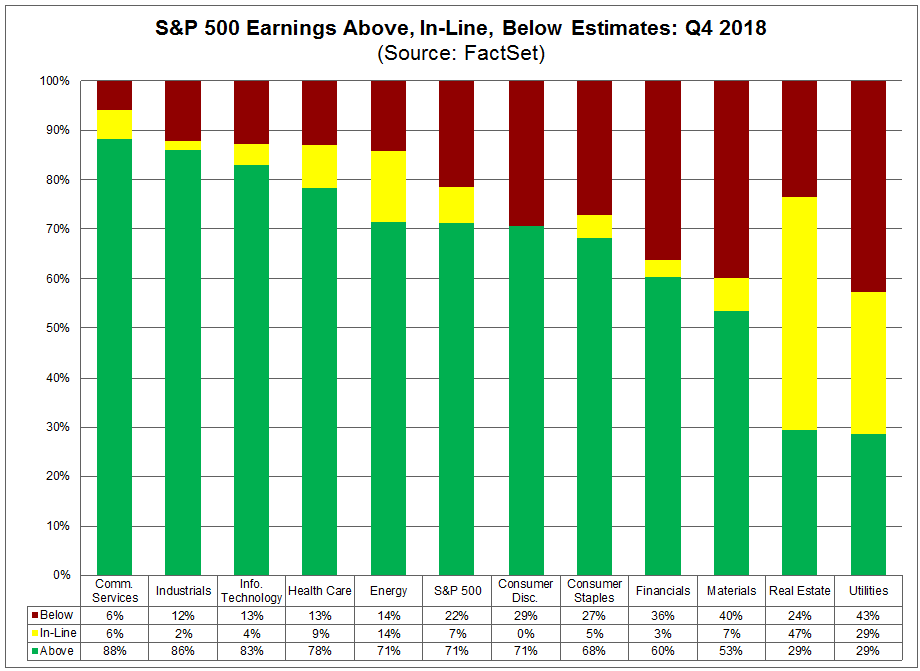

(Earnings Data: FactSet)

Going forward, trader direction is likely to be influenced by corporate earnings season in the U.S. (which has officially reached its mid-point). Thus far, roughly 235 companies in the S&P 500 have reported their quarterly results. Earnings growth is currently visible at a rate of approximately 18% on an annualized basis, and this is above the prior estimates calling for earnings growth of 15.5%. To date, roughly 71% of the S&P 500 companies that have reported have beaten analysts’ expectations. This is strongly above the historical averages of 64%.

(Commodities Price Data: AskTraders.com)

Commodities traders continue to travel on a roller coaster ride, and macro data in the next few weeks could make this volatility even more pronounced. Slower demand levels led to the drastic fall which completed at the end of 2018, and commodities bulls have attempted to start buying in at the lows. Resistance levels from December have officially broken, and we are also trading above the 50-day moving average in WTI crude prices. These are both bullish events, which suggests that we could see further rallies into the upper $50s.

This stock market analysis was originally featured as part of the MarketBulls.net daily trading commentary.