Access to safe water and sanitation is a fundamental human right under binding international law. Yet today, a global water crisis still persists. 2.2 billion people—or 1 in 4—still lack access to safe water and 3.5 billion people—or 2 in 5—lack access to safely managed sanitation.

While gains have been made over several decades, the effects of climate change have become a large and looming factor, halting progress made. Though the role of the public sector remains paramount in addressing the crisis, private impact investment has recently also emerged as a powerful tool.

Investing in household water and sanitation solutions

Impact investing focuses on generating positive social and environmental impact while seeking financial returns. In the realm of water and sanitation, investment plays a pivotal role in supporting innovative solutions, especially at the household level. Among low-income consumers, at least 600 million people could access water and sanitation products, services and upgrades if financing was available, equating to what WaterEquity estimates as $35 billion of market demand over the next decade.

WaterEquity has approached this market opportunity through an investment strategy focused on providing debt capital to financial institutions in emerging markets to expand water and sanitation lending. These financial institutions use this capital to grow their water and sanitation microloan portfolios, as well as to on-lend to local enterprises delivering water and sanitation innovations, products and services.

Since our start in 2016, WaterEquity has deployed more than $360 million in capital to this strategy across four private investment funds, reaching more than 5 million people with increased access to safe water and sanitation.

Over 93 percent of the low-income end-clients taking out these microloans are women. This is no accident, as the funds have specifically targeted women beneficiaries by integrating gender into our investment and decision-making processes. And the microloans are repaid at the average rate of 97-99% within 12-24 months. Ensuring equitable access to safe water and sanitation cannot be accomplished without giving women the power and the capital to solve for their futures.

Photo courtesy of WaterEquity/water.org

Investing in climate-resilient infrastructure

Financing the “last mile” of water and sanitation access at the household level will only take us so far in reaching the billions affected. There is also a tremendous need and market opportunity for sustained investment in potable and wastewater infrastructure seeking to increase access to water and sanitation services, improve water quality and mitigate the impacts of water scarcity.

Moreover, with traditional infrastructure often vulnerable to damage from extreme weather events, investment in resilient systems is essential for ensuring sustainable access to water and sanitation services.

By investing in climate-resilient infrastructure, WaterEquity’s Water & Climate Resilience Fund aims to reach 15 million people with water and sanitation access, and indirectly benefit millions more through improvements in water quality and scarcity.

Investments include government tendered projects such as the construction of decentralized water treatment plants, the upgrading of existing infrastructure to withstand extreme weather events and the implementation of smart water management systems. The Fund will also invest directly in growth companies that are developing and deploying innovative technology and services within the sector. These projects and companies enhance the reliability and efficiency of water and sanitation systems at scale, while also contributing to the overall climate resilience of underserved communities.

Conclusion

Impact investing has the potential to transform the landscape of water and sanitation, addressing the complex challenges posed by the water crisis, climate change, and gender disparities. By supporting innovative household solutions and investing in climate-resilient infrastructure, impact investors can contribute to the Sustainable Development Goals and improve the well-being of communities around the world, aligning values with the potential for financial returns.

This holistic approach not only addresses immediate water and sanitation challenges but also builds resilient communities capable of withstanding the impacts of a changing climate. Through strategic and socially responsible investments, we can ensure a future where safe water and sanitation are accessible to all.

Elan Emanuel is the chief investor relations officer at WaterEquity. Elan is responsible for mobilizing investments and partnerships with a broad portfolio of investors to accelerate WaterEquity’s impact addressing the global water and sanitation crisis. WaterEquity emerged out of Water.org and was cofounded by actor Matt Damon and Gary White.

Investing beyond numbers: paving the path for a sustainable future

Gone are the days when investing was solely about maximizing profits. Today, it’s about making a meaningful impact, and therefore individual investors are increasingly seeking to align their financial goals with their personal values.

The attraction of Environmental, Social, and Governance (ESG) investing stems from two primary aspects. First, some individual investors prioritize their ethical values and social responsibility over maximizing profits. In other words, they are willing to forgo some profit to contribute to societal good. Second, profit-driven investors believe companies that focus on ESG responsibility are likely to be better managed and more adept at foreseeing and reducing risk, making them better potential long-term investment opportunities.

Struggles with Sustainability

While sustainable investing is gaining traction, many retail investors still do not consider ESG when making investment decisions. This is driven by several underlying factors, including lack of education about ESG, the appearance of limited investment options, accessibility and consistency in ESG data, and combatting short-termism, to name a few.

Lack of education

One of the most common hurdles in ESG stems from a lack of education—a lack of familiarity with and understanding of what investment options are available to them. For example, a study from owlesg.com points out that 46% of respondents stated that the main reason they don’t consider ESG investments is a lack of familiarity. This also study highlighted that nearly 28% of respondents didn’t know how to determine whether an investment was ESG-friendly, and just 15% noted performance concerns as a reason for not investing in ESG.

This study highlights that retail investors need help understanding how to learn about and research ESG investments, not necessarily performance concerns.

Limited investment options

According to a study by the Wisdom Council, nearly six in ten retail investors are unaware that they can invest in a way that positively contributes to ESG, and four out of five surveyed believe they have a key role to play in protecting the environment.

Data accessibility and consistency

Another key hurdle for individual investors is the lack of easy access to ESG data through a single source. Instead, many companies publish “sustainability reports,” requiring investors to fumble through pages of jargon, often leaving them more confused than when they started.

To further highlight this point, according to frameworkESG.com, nearly 600 different ESG ratings are published globally, making it exceedingly difficult for investors to make sense of varying guidance and frameworks.

Short-termism

Short-termism is characterized by a myopic focus on immediate financial gains at the expense of long-term sustainability and is another obstacle to sustainable investing. Many companies prioritize short-term profits to meet quarterly earnings targets, often neglecting long-term investments in sustainable practices.

Investors can advocate for corporate accountability and encourage companies to adopt a more holistic approach that considers both financial performance and environmental stewardship; however, this is more commonly done from an institutional level.

In many cases, short-termism can be difficult but possible to combat. For example, a recent Harvard Business Reviewarticle points out that when Paul Polman became the CEO of Unilever, then an underperforming consumer goods giant, he immediately ended quarterly earnings guidance. Instead, became explicit about his commitment to a long-term strategy rather than focusing on short-term profits.

That guidance led to an exodus of short-term-focused investors, thereby attracting more patient capital which is critical to sustainability efforts.

Empowering investors to make an impact

To make a difference, individual investors need to adopt a strategic approach that combines financial returns but also consider social and environmental impact.

According to a study by the Morgan Stanley Institute for Sustainable Investing and Morgan Stanley Wealth Management, approximately 77% of individual investors worldwide are “interested in investing in companies financial returns while also considering positive social and/or environmental impact.”

Studies show that investing in ESG companies does not affect returns. According to a study from Morningstar, it found no risk/reward trade-off to investing in ESG companies – in other words, retail investors do not have to compromise returns in exchange for building a portfolio of ESG companies.

So what does this all mean?

It is clear that investors are not concerned about sub-optimal returns with ESG investments and empirical data indicates the same. Instead, individual investors need to become more familiar with ESG. They don’t know how to make sense of the labyrinth of ESG rating methods, how to access and read them, and what ESG-friendly investment options are available. ESG investing has just become too complicated for many retail investors.

Join ESG communities and events

To engage with fellow ESG enthusiasts and professionals, consider joining online and offline communities and events. These platforms provide valuable opportunities for networking, learning, and collaboration. Among the most active and diverse are:

The ESG Investing Group on LinkedIn a community for ESG investors to exchange news and perspectives.

The ESG Circle on Meetup a local community where ESG enthusiasts can connect and socialize.

Familiarize yourself with ESG standards and ratings

To grasp ESG concepts, start by acquainting yourself with the various standards and ratings that assess and benchmark ESG performance across sectors, regions, and themes.

Among the most prevalent and reputable are:

The Global Reporting Initiative (GRI)

Sustainability Accounting Standards Board (SASB),

Task Force on Climate-related Financial Disclosures (TCFD),

UN Principles for Responsible Investment (PRI). These frameworks offer guidance, metrics, and leading practices for reporting and disclosing ESG data to diverse stakeholders.

Understand ESG investing approaches

Generally speaking, there are 3 common ESG investing approaches: Values-based, ESG Integration, and Impact Investing. Retail investors must know these approaches compared to traditional investing.

1. Values-based investing, or Socially Responsible Investing (SRI), is one of the most well-known ESG investing approaches. This approach involves avoiding investments in specific sectors or companies, like tobacco, firearms, or fossil fuels – colloquially known as ‘sin stocks.’ This strategy appeals to retail investors who want to avoid supporting businesses they may find objectionable.

Investors can easily get exposure to funds that avoid ‘sin stocks.’ For example, VFTAX, Vanguard FTSE Social Index Fund, is a mutual fund screened for specific environmental, social, and corporate governance (ESG) criteria.

2. ESG integration is a more contemporary investment strategy pioneered by major investors like pension funds and endowments, but it can also be applied by individual investors. ESG integration strategies are usually more aligned with broad benchmarks, offering some exposure to economic sectors rather than entirely excluding specific sectors they may deem unacceptable. Put simply, these strategies do not avoid specific industries entirely; rather, they limit their investment exposure.

For investors just getting started in ESG investing, an ESG Integration approach may be the most practical to implement.

3. Impact investing is a more direct approach that involves investing money to achieve a specific positive outcome. Examples include offering loans to low-income homebuyers, funding projects to cut factory air pollution, investing in carbon credits, or even buying shares in a company to influence its policies.

While it may be difficult for individual investors to provide funding or influence a company’s policy directly, one example is Vanguard’s Bailie Gifford Global Positive Impact Stock Fund Investor Shares, VBPIX, which is an “actively managed fund that seeks to invest in global high-quality growth companies that can deliver positive change in one of four areas: Social Inclusion and Education, Environment and Resource Needs, Healthcare and Quality of Life, and addressing the needs of the world’s poorest populations.”

Bringing it all together

Empowering every investor to embrace sustainable investing requires addressing challenges related to transparency, data quality, regulatory compliance, and short-termism. By fostering a culture of accountability, promoting education, and providing accessible investment options, we can bridge the gap between values and finance, paving the way for a more sustainable future.

The Sustainable Finance Podcast is a weekly program featuring conversations with sustainability thought leaders such as cleantech entrepreneurs, VC investors, CEOs, NGO executives, and creators of the ESG indices and analytics platforms.

Radhika Shroff is managing director, impact investing/private equity at Nuveen, one of the world’s largest institutional investors. For Radhika and her Nuveen private equity team, their investment thesis is rooted in addressing two critical and inextricably linked problems: inequality and climate change.

With impact investing at an inflection point in 2024, I asked Radhika to explain how tackling these two issues creates attractive impact investment opportunities outside of traditional developed markets while offering investors stable, competitive returns — a process that also identifies companies best positioned to grow and lead in the decades to come.

Paul Ellis: Radhika, in the current market, what are some of the key trends in impact investing that you and your team are paying attention to in 2024?

Radhika Shroff: I have some key trends in mind, and as I thought about them, I hope they are not wishful thinking but are actual trends. We are focused on investing in growth stage businesses that are either solving a climate issue or an inequality issue.

The reason we’re focused on those two sectors is because we do believe that they’re inextricably linked, and that as the world warms, different populations are going to be impacted in different ways. So, for example, me living in an apartment building in New York City, I’m going be impacted very differently from climate change than a small holder farmer living on the coast of India. I’m also going be impacted very differently than somebody living in affordable housing also in New York City.

So we’re really focused on that confluence and saying it’s not just that we need to think about how to get more carbon dioxide out of the air. We do need to do that, but we also need to focus on ensuring that populations, wherever they are in the world, are resilient to climate change. And we believe that inequality plays a big factor in that.

The first broad macro trend that we’re seeing is that asset allocators are starting to see impact private equity as a mainstream asset class. And importantly, I think they’re also starting to see that you can invest with an impact fund and still expect the same returns that you expect from all of your mainstream private equity funds.

And not only can you expect them, you should expect them. The thesis behind this is that we’re not going to solve the world’s biggest problems without being able to attract commercial capital. And the only way we can attract commercial capital is by showing commercial capital that we can return private equity returns with our impact investments. And that impact and financial return are not mutually exclusive. They can actually go hand to hand.

We’re seeing through our efforts, our fundraising efforts, etc., and increasing recognition, that a fund like ours should be put on the same level as any other private-equity fund out there that might be looked at in terms of returns.

PE: I think those are very important points to make right up front because as you say, a lot of investors over the last 50 years or so have shied away from the private markets in terms of impact investing for a number of reasons. But what unique benefits can impact investing offer from both a financial and environmental and social impact perspective?

Radhika Shroff

RS: Private equity is really the tip of the spear when it comes to driving impact in companies. So, as we know, private equity is longer term than public markets, and we have a five to seven year investment horizon. And so we’re able to sit at the table for at least five years working hand in hand with the company, the management team, the other shareholders, and we’re typically minority shareholders, to say not only how can we drive financial performance, but how can we also drive impact?

One example: We recently invested in a company called Power Takeoff, a company that drives energy efficiency in the small business sector, and its clients are utilities. The small business sector of the United States is typically underserved when it comes to energy efficiency solutions. And so we were super interested in that piece of it. As I’ve noted, we not only like to provide our capital, we like to provide engagement as well to help companies meet their goals.

With Power Takeoff what we’re doing is we’re leveraging the know how of our broader real estate platform, in particular, our affordable housing platform, which is the largest in the United States, and saying: How can we help this company increase its revenue, not only by targeting just small businesses, but also by targeting small business energy efficiency in low-income communities?

Right there you see an example of private equity being particularly impactful when it comes to driving both revenue as well as impact. And you also see coming to fruition our thesis that we want to make sure that low-income communities are not left out of the climate transition.

PE: So this is an example of a dual purpose focused on a particular investment idea and a company that offers these kinds of services. And you can apply it, as you’re saying, across a broad population of opportunity because of your engagement with the sector of the economy that it’s based in.

RS: Yes. What we’re saying is as private equity investors we can be patient, right? We do need to exit, but we can be more patient. And we can engage in such a way that drives impact. And if the impact is linked to the core revenue model of the business, as we drive more impact, we’re also driving more revenue. And that is really our goal as private equity investors.

PE: How do you and your team evaluate the investments that you’re in? There’s clearly a very-well-thought out process.

RS: I noted that we have a very well-thought-out impact thesis. We invest in either climate solutions or income inequality, and we love it when the two come together, when we invest in a business where we can help drive that equitable transition. But we’re like any other private equity fund. We look at the growth dynamics of the business.

We look at profit, profitability, we look at margins. We look at the segment, competition, we look at management teams. We look at the risk of the countries that we’re looking at. We look at competition and, importantly, we care deeply about exit optionality. We know being private equity and impact investors for over a decade that our industry needs to show investors that companies can be exited, and they can be exited in the same way, with the same velocity as a non-impact focused company. And so we’re really focused on exit.

I would say the way we look at our companies is the same way as anybody else, but we go a step further because we’re impact investors. We say, what is the “but for” of this company, if this company did not exist, what are the other options that the end consumer or the end segment has to solve this issue for themselves in a commercial way?

And this “but for” conversation is key and happens to be one of the most lively conversations we have on the team when we’re thinking about an investment because every single person on our team wants to be intellectually honest around the fact that this is a company, as it grows, it’s actually increasing its positive impact on the world more than not.

Rajani Srichandana, a client of Annapurna Finance.

One example: We invested in an Indian microfinance institution called Annapurna Microfinance. Now, this is a company that served around 1.5 million female entrepreneurs with working capital loans so they could grow their business when we first considered investing. And we said, okay, “but for” our investment, what would actually happen here? Where else could these people go?

This is a company that happens to be going to some of the hardest to reach places serving women who are underserved from a working capital standpoint with well-priced loans. Since we’ve invested, this company has doubled in size and we are likely going to be able to exit in the next 12 to 18 months at really strong returns. And we’re saying, look, we invested, it’s doubled in size, and therefore it now serves 2.5 million women with working capital—not loans. And that’s where we see our investment going hand in hand with the impact that we’re trying to drive.

PE: That’s very impressive data. Can you give us the timeframe in which this has happened?

RS: We’re really proud of it. We invest globally, largely in the United States and India, and some of us on the team have been in investing in India for over a decade and driving the same level of returns that you would see in the United States on U.S. dollar terms. In Annapurna, we made the investment in March 2021. It was a really difficult time to be making investments in India. That was right before wave two of Covid.

But because we know the sector so well, and because we know the management team so well and the business model, we knew that if we made the investment at this moment in time, we would be strengthening the company’s balance sheet at a very, very good valuation. And we knew that those dollars would go towards making more loans to underserved communities. The company grew from 1.8 million clients to 2.5 million clients in the last three years.

PE: So is this part of your methodology that you and your team use in scrutinizing every type of investment that you’re looking at in these markets?

RS: Yes. We really like when we’re serving low-income, underserved clients, especially on the financial inclusion piece, which is largely in an emerging markets India play, but we also care deeply about climate. So again, for example, In India we invested in a company called Ecozen, a company that manufactures and markets IOT enabled solar irrigation pumps and cold storage, largely for small holder farmers who are living in areas that could be off the grid or have unreliable utility service. And this helps them keep their crops irrigated and store their crops for longer periods of time in order to increase their income.

Ecozen photo

And in that one investment, what we’ve done is invest in a climate mitigation, a carbon dioxide reducing product. In fact, that one company in one year alone, reduces carbon dioxide emissions by 500,000 tons a year. And we’re helping small holder farmers with the reliability of being able to grow and store their crops. So it is really emblematic of what we’re doing.

And by the way, all of these companies in our Fund One, they’re on average growing at 40% to 50% a year. What that really means to us is that we’re investing in commercially viable, profitable companies with strong profit margins that are serving an underserved segment of the community that really needs these basic services. And that’s really the sweet spot of what we’re doing.

PE: How do these underserved communities in these economies around the world react to a company like Nuveen coming into their community and offering this type of capital infusion and long-term investment strategy? That must be an extraordinary process and if you could just share with us some of the reactions that you get from the local people, that would be very helpful.

RS: Sure, absolutely. We have a really lovely video of clients in Annapurnatalking about what Nuveen has done for their lives. But I’ll tell you, we’ve been investing in these emerging economies for over a decade. We’re pretty well known. When we come to the table and say we want to look at this business, people are excited and happy. Because they know a couple things.

One is that we are intellectually honest around caring about impact. And so that gives management comfort that we’re not going to be there just driving profitability for profitability’s sake. We want to make sure that profitability is coming in lockstep with the impact. And so it gives them some sense, OK, it’s this big U.S. firm, who are they going to be? What are they going to be like? They know from our reputation that we are going to be there to support them on the impact side as well.

The second thing, they know we can really help them scale. We typically come in, we’re not venture investors, but we’re also not TPG Rise. We are there to help them with what we call the missing middle: we believe there’s a lack of commercial investors in that stage of the company development from when it’s proven the commercial viability of its product or service to what is completely scaled to be able to exit to the public markets. Or to be able to do a strategic sale or sell to a TPG Rise for example.

And they know that we’ll be there, and we know how to help them scale. I think we see that our pipeline outside the United States is just as exciting as our pipeline inside the United States and that’s why we’re building a balanced portfolio.

PE: That’s terrific news. A lot of people in the private markets in developed economies look at the potential risks of these types of investments and shy away from them. What you’re saying is that you have dug much deeper into the process of these economies and the people that you’re working with and come up with ideas that are leveraging opportunities in those economies and at the same time de-risking the longer term investment strategy. Am I on the mark?

RS: Absolutely. And it takes a great deal of experience to be able to do that. Like it’s pattern recognition. It’s the people you know understanding, you know you can’t predict, but you can understand how currencies move, the macro environment, we’ve done all that. We’ve been doing it for over a decade.

And as I said, and I can’t say this enough, the things that we see in India, in particular the growth that we’re able to see there, the returns we’re able to drive are on par, if not better, than some of the developed economies we look at.

PE: Are there other developing economies around the world that Nuveen is looking at or already engaged with that you can share with us?

RS: We look at all of the largest economies. So, some of the larger countries in Southeast Asia and Latin America. We actually have an investment in a payments company in Latin America that essentially provides mom and pop shops in rural areas in Peru with a handheld device so they can turn into mini bank branches.

So this is really financial inclusion. You are going into the Andes Mountains. You’re handing a store owner a handheld device and a customer that lives in that neighborhood doesn’t have to travel 3 hours to the nearest bank branch.They can do simple financial transactions at this mom and pop shop in their neighborhood.

And this mom and pop shop, which is owned often by a female entrepreneur, is able to increase the revenue of her shop by 20% to 30%. And these investments outside the United States are made after deep (review); I had known this company for 10 years before I made the investment.

Financial inclusion is something we know really well. So we don’t take it lightly. We know that investing outside the United States has its macro risks. But I think if you have the right team that has done it for a long time and knows how to underwrite for those risks to the extent possible, you can end up with really good, strong risk adjusted returns.

PE: Radhika, where can people go to learn more about private equity impact investing at Nuveen?

RS: You can find us on the new Nuveen website. We have some really interesting thought leadership pieces there, where we talk about why we invest in India, why we invest in companies that are focused on decarbonization of buildings. And anyone can find me on LinkedIn.

GreenMoney Interviews: Kirsten James on Ceres’ Valuing Water Finance Initiative

As the global water crisis worsens, so do financial risks facing companies and their investors. Kirsten James, senior program director of water at the sustainability nonprofit Ceres, answers questions from Cliff Feigenbaum, Founder and Managing Editor of GreenMoney about the Valuing Water Finance Initiative, which is a global, investor-led effort driving companies to prioritize water risk and act as responsible water stewards in their operations and supply chains.

Cliff Feigenbaum: What work has Ceres done related to water?

Kristen James: Freshwater is essential for people, ecosystems, and business. Growing water scarcity and pollution is threatening these systems and slowing the pathway to a climate resilient future. Research shows we’ll be unable to meet even 56 percent of global water demand by 2030. No industry is immune from financial risks stemming from this crisis.

Seeing this writing on the wall, we’ve spent more than a decade establishing the business case for the private sector to act on water risk. We’ve worked closely with investors on integrating water risk into their investment decisions and developed resources to help them understand water risk in their portfolios. Our research and corporate benchmarking has shed light on industry practices threatening freshwater supplies and how companies are responding. This information has empowered investors with the guidance and the data they need to evaluate how companies are managing water risk. Cliff: How did this work pave the way for the Valuing Water Finance Initiative?

Kristen: Through this pioneering work we did on water risk, we saw the need for ambitious action to match the scope of the water crisis and the systemic risks affecting communities, nature, and economies. We developed the Valuing Water Finance Initiative, aimed at driving companies to make water risk and water management a priority in their business strategies. Because water is key to their success as a business.

This work is hitting home with investors and the initiative has taken off. Just two years after we launched it, nearly 100 investors representing more than $17 trillion in assets have joined. These investors are committing to engage with 72 large companies from four water-intensive industries—food, beverage, apparel, and high-tech—on their water management practices.

Cliff: How does Ceres see investors’ efforts through the Valuing Water Finance Initiative leading to action on the ground?

Kristen: Companies aren’t just at risk from dwindling water supplies and polluted water, they’re making these risks worse by mismanaging and undervaluing water resources. Investors play a crucial role, as shareholders of companies, in compelling businesses to preserve and protect the water supplies they depend on.

Through the Valuing Water Finance Initiative, investors are encouraging companies to develop holistic water management strategies by focusing on six Corporate Expectations for Valuing Water. These expectations set ambitions around the full range of water issues that large companies should meet by 2030. This timeline is critical to slowing the pace of deteriorating water resources across the globe and meeting the United Nations 2030 Sustainable Development Goal for Water (SDG6).

Investors, through dialogues and, in some cases, shareholder resolutions and other strategies, are making progress working with companies on taking important steps, such as conducting water risk assessments in their supply chains and developing strategies to act on this critical information. Managing water risks in their supply chains is critical because they make up a significant portion of where companies depend on and have an impact on water.

Cliff: How are you gauging companies’ progress?

Kristen: Ceres’ recently released benchmark report assesses how the 72 focus companies are performing against the Corporate Expectations. It is an important resource for investors as they continue to engage with companies because it provides more context around companies’ water stewardship efforts—where they are excelling, where they are lacking, and how they can accelerate or expand their efforts.

The analysis, which we developed using publicly available company disclosures, offers a snapshot of where each company is on its water stewardship journey. No company is leading the way or close to meeting the Corporate Expectations lined out by investors, but we were encouraged to see 11 of the 72 companies making substantial progress. However, with only seven years until 2030, there is significant work ahead for most of the companies we assessed.

Irrigation pipe photo by Surachat, courtesy of Ceres

Cliff: How can companies step up their actions in the face of worsening water scarcity and pollution and related financial risks?

Kristen: Results vary by company and industry, but our research highlighted key areas for improvement. For example, many companies are using less water, but they need to make similar progress in addressing the impact their operations and their suppliers’ operations have on polluting water. This will help them bridge other gaps, such as protecting the ecosystems that are vital to freshwater supplies and ensuring that the communities where they operate and source commodities from have clean water.

Most companies can also do better ensuring that their public policy activities support sustainable water management. Advocating around water issues with governments, businesses, and civil societies can strengthen and broaden companies’ water stewardship efforts and impacts.

Many companies have made notable strides. They are demonstrating innovative and effective water solutions, including working with other stakeholders to address shared water challenges. Peers can learn from these examples in building their own water management strategies.

Cliff: How can investors accelerate action?

Kristen: In our discussions with investors, they have said they will look to companies to implement and advance leading practices, starting with risk assessments of their entire value chains and setting targets that home in on high-risk watersheds. Investors will also consider whether companies’ boards and senior leadership oversee water management strategies and integrate water risks and opportunities into strategic business planning for direct operations and supply chains.

Companies must take a leading role in tackling water risks impacting global water resources and economic security. Investors can fuel progress by taking an active ownership approach and using their power of influence to urge companies to understand their water vulnerabilities and take deliberate steps to avert financial fallout from the unfolding water crisis.

About Kristen:

Kirsten James directs Ceres’ strategy for mobilizing leading investors and companies to address the sustainability risks facing our freshwater and agriculture systems. Her work includes leading the Valuing Water Finance Initiative, an investor-led effort which seeks to drive corporate action on water-related financial risks. Previously, Kirsten served for five years as the director of California policy and partnerships at Ceres.

Prior to Ceres, Kirsten worked for nine years at a regional water resource-focused NGO, as their Science and Policy Director. She graduated with a bachelor’s degree from Northwestern University and a master’s degree in environmental science and management from the Bren School at University of California Santa Barbara.

Thursday is National Pet Day in the United States. In addition to the added attention the day focuses on our four-legged companions, it’s a good time to note the increasing interest in bringing animal welfare into a more prominent role in impact investing.

An analyst team at AskTraders, a London-based financial services platform, decided to delve into animal welfare, recognizing that cruelty-free investing was becoming a hot topic among its online community.

Here are seven investments that these analysts say you should consider if animal welfare is one of your impact investing criteria. They complied the recommendations after incorporating the guidance offered by the nonprofit organization Cruelty Free Investing and the Caring Consumer Database operated by PETA.

Beyond Meat

Probably the most obvious choice in this analysis, Beyond Meat

BYND

is a Los Angeles–based producer of plant-based meat substitutes. Founded in 2009 by Ethan Brown, the company’s initial products were launched in the United States in 2012. The company went public in 2019, becoming the first plant-based meat company to go public.

The stock jump from its IPO price of $25 a share to trade above $222 that first year, But the euphoria wore off soon after: The stock today trades near $7.

Beyond Meat photo

“Some of the early-stage projections for growth were overinflated, and traditional valuation models always deflate stock market bubbles in the end. The price drop also ties in with other cruelty-free stocks coming to the market and offering alternative options for those looking to invest in the sector, the analyst team wrote.

But they point out that Beyond Meat is still a standard bearer for the cruelty-free sector, and many will be considering buying in at levels where it can be argued to be undervalued.

Microsoft Corp.

Perhaps the least intuitive pick on the list, Microsoft

MSFT

is not involved in any activities that harm or exploit animals. AskTraders noted the company is working to preserve the planet for all its inhabitants, animals and humans. It aims to be carbon negative by the end of this decade by cutting emissions, and is also removing its historical carbon emissions by 2050.

“Microsoft is not a vegan trailblazer in the sense that Beyond Meat is, but it illustrates how wide the spectrum of ethical investing extends.,” the team said. “If you’re looking for a cruelty-free stock that is also a sensible investment option, then market giant Microsoft fits the bill.

The stock is up about 70% over the last three years and remains near an all-time high at $425.

Ingredion Inc.

Ingredion

INGR

provides plant-based ingredients for food, beverages, pharmaceuticals and beauty products. It makes the cruelty-free investing list of companies that don’t exploit animals and the Ethisphere list of the world’s most ethical companies – scoring high on many criteria such as diversity and inclusion and transparency, as well as animal welfare.

The company also aims to help customers replace synthetic ingredients with naturally derived solutions and makes its plastic packaging more biodegradable and earth-friendly.

“The share price of INGR is at the same time relatively stable, which makes it a good pick for beginners looking to gain exposure to the sector, rather than a speculation-based, roller-coaster ride,” AskTraders said.

The stock has hung around the $100 level over the last three years and is just below its recent high. In addition to the relative stability of its stock price, the company has paid a steady dividend over the year, with a current yield of 2.8%

Colgate-Palmolive

The AskTraders analysts admit that Colgate-Palmolive

CL

falls into a ‘gray area’ on the animal welfare front. While the company has since 1999 maintained a voluntary moratorium on animal testing of its adult personal-care products, certain of its products must by law meeting testing protocols that do involve animals.

So it doesn’t make PETA’s list of companies that do not test on animals, but it is included in that group’s list of companies working for regulatory change.

Colgate-Palmolive Innovation photo

“Some credit goes to Colgate-Palmolive for actively working for the replacement of animals with non-animal methods, and for also releasing to PETA all information about tests and what it has done to avoid them,” the analysts said.

The stock is part of a staid group of consumer staples companies that are considered defensive plays for the most part by Wall Street. The stock is up just under 8 percent in the last three years. It’s dividend yield is 2.3%.

Accenture PLC

The global professional-services company is on the cruelty-free investing list of safe investment companies. Accenture

ACN

does well on other ESG criteria, such as equality, environmental impact and good governance, and is one of the world’s most ethical companies, according to Ethisphere.

“Accenture isn’t an exciting hyper-growth stock, but has a role to play as part of a well-diversified cruelty-free portfolio. By helping to smooth out overall returns, it can act as a counterweight to more volatile stocks, and allow investors to stay in high beta positions during periods of market uncertainty,” the team said.

The stock is up about 15% over the last three years, but well off its high over $400 at the start of 2022. Its dividend yield is 1.6%.

Oatly Group

Oatly

OTLY

seems a controversial pick, given prior questions over the company’s business practices and its reliance on a $200 million stock sales to Blackstone Group, which has been under fire for other investments that are not ESG aligned.

But the Swedish-based producer of alternatives to dairy products that grew out of research labs at the world-renowned Lund University has been successful, growing to be available in 60,000 retail stores and 32,200 coffee shops around the world.

“The ethical concerns surrounding Oatly represent significant growing pains, but the firm’s vegan credentials are beginning to look stronger,” the analysts said.

It’s stock is certainly not for everyone. At $1 a share, it is light years below its 3-year high of $26.

“However, the strong brand recognition makes the stock an interesting proposition for value investors with a long-term view and a desire to tap into the vegan sector,” AskTrader said.

U.S. Vegan Climate ETF

The US Vegan Climate ETF

VEGN

tracks the Beyond Investing U.S. Vegan Climate Index. That index screens large-cap U.S. companies using a variety of ESG criteria. It gives additional weighting to animal harm issues and animal exploitation, as well as fossil fuels, environmental damage and human rights.

“The total expense ratio of the VEGN ETF is 0.60%, which is in line with the industry average, so those who buy it are getting the additional screening of animal cruelty stocks at a cost-effective rate. It also comes with all the functionality advantages of ETFs and offers exposure to a wide range of cruelty-free companies in just one trade,” the analyst team noted.

The exchange traded fund is up about 20% in the last three years and is trading just below its 3-year high near $47. It pays a small dividend that yields 0.6%.

All industries are prone to hectic merger and acquisition activity. We covered a number of these events in the pharmaceutical industry in previous entries. Silicon Valley has reached a peak – sounds like an oxymoron! – with the giants acquiring relatively new, expensive and promising companies.

This year, Cisco

CSCO

paid $28 billion for enterprise cloud protection company. Splunk’s president and CEO will join Cisco’s leadership team. In a similar spirit, Alphabet

GOOG

acquired Photomath in 2023 for about $550 million, enriching its founder considerably.

Microsoft

MSFT

, the Office Suite king, sits on its giant pile of cash waiting for its next opportunity after acquiring Activision in 2023 for $69 billion. Before the deal took place, the CEO was in line to take in $500 million.

These costly transactions show that in these fast-moving industries, money flows freely and founders reap massive financial rewards. Huge piles of money make most people happy. As Caesar said, we must take the current when it serves.

Recently, Elon Musk got into a dispute with OpenAI. Musk’s argument is that he personally financed OpenAI and had an agreement that the company would stay nonprofit and share its technology. Now the company is pushing for profit. Musk sees this as a betrayal.

The Musk-OpenAI dispute is much closer to old-time disputes between management and “corporate raiders.” Among the biggest of such battles was Icahn and Clorox

CLX

, $11.7 billion, 2011. After becoming its biggest shareholder, Carl Icahn fought with the Clorox board.

Musk’s OpenAI dispute follows his long, contentious acquisition of Twitter, now X. Now part of history, Musk’s Twitter acquisition uncovered the venom of his business enemies and even his newly acquired employees, some of whom profited considerably.

Elon Musk

After the Electric Car King indicated his interest in acquiring the social media giant, the anti-Musk gang lined up, saluted and started firing. A bunch of politicians, some of whom had received hefty gifts from Musk, shuddered to think of what the acquisition would reveal about how Twitter favored certain candidates for office. They turned on their benefactor.

Some employees and executives at Twitter opposed the purchase, fearing that embarrassing practices would be exposed. If nothing else, the management style of the company would be held up for ridicule. They turned on Musk in a nasty public fit of anger.

As the Twitter situation came to a boil, people under the Twitter tent, especially rights activists, approached Apple

AAPL

, Disney

DIS

, Coca-Cola

KO

and others grumbling that the post-acquisition Twitter might feature racist posts and hate speech. They recommended cutting advertising. Talk about disloyalty!

Tesla

TSLA

and Space X have raked in billions from the federal government. Musk rubs shoulders with the top echelon in Washington. But, when critics came after him for taking over Twitter, his elected friends ran for cover or sniped at the multibillionaire.

Like Julius Caesar, Musk is a lightning rod. Jeff Bezos, fellow billionaire and founder of Amazon

AMZN

, has had a long public feud with Musk over a range of issues. Musk and Meta’s

META

Mark Zuckerberg have also gone at each other publicly. President Biden, head of the political party that strongly advocates for electric cars, took shots at Musk for a variety of reasons, including Twitter.

As Brutus said, “Chew upon this.”

On top of his detractors, Musk’s massive wealth sent a signal that a hefty premium would be demanded for any acquisition. Warren Buffet has always had to pay significant premiums. In his 2022 acquisition of Allegheny for $11.6 billion, the Oracle paid a premium of 16%. Precision Castparts was acquired for $37 billion in 2016, which included a 21% premium.When he bought Burlington Northern Santa Fe Railroad, the premium was 31.5%. Musk’s premium for Twitter was estimated at 38% in one of the largest acquisitions ever made and puts him at the top of the list of premium payers.

So, we see from these events that even money does not seal friendship. Plenty of people smile, appear to be friends and stab you. Win or lose any of these public battles, Musk remains a Caesar-like target.

In this bi-weekly series, Equities News in collaboration with Till Investors provides readers with an overview of specific mutual funds and ETFs within the sustainable investing marketplace. The goal is to help readers identify investment funds that meet their risk profile, impact interest and investment goals.

Today, we’re providing insight into a sustainable fund that focuses on bonds – the lower-risk, lower-return alternative to stocks. While the vast majority of ESG funds invest in stocks, ESG fixed income funds are carving out a niche amongst investors as well. But what does a sustainable bond fund look like, and who is it a good fit for? Let’s dig in and find out by taking a look at…

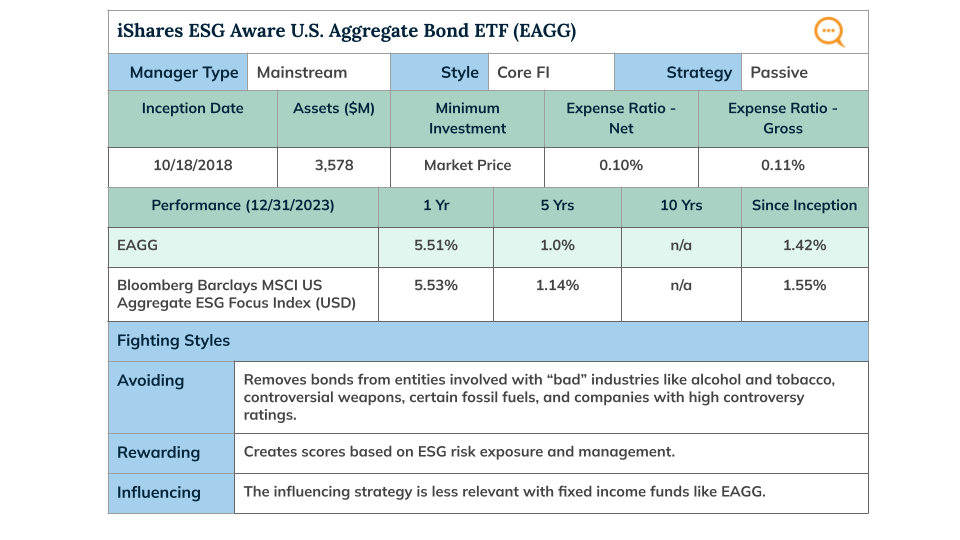

iShares ESG Aware U.S. Aggregate Bond ETF (EAGG)

Who is iShares?

iShares is a brand of funds managed by Blackrock. Blackrock is one of the world’s largest asset managers with a diverse lineup of ESG funds. Their largest ESG bond fund is the iShares ESG Aware U.S. Aggregate Bond ETF (EAGG), with over $3.5 billion in assets. Like most iShares products, this fund is structured as an ETF, and like most ETFs, it is designed to follow an index – in this case the Bloomberg Barclays MSCI US Aggregate ESG Focus Index.

What does the EAGG bond ETF offer?

The index this fund tracks is based on the broadest market of U.S. investment-quality bonds, known as the Barclays U.S. Aggregate, or “the Agg.” It is designed to represent the broad investment-grade bond market in the U.S., including Treasuries, mortgage-backed bonds, asset-backed bonds, and corporate bonds. The ETF structure means that management costs are very low for this fund. At the same time, passively following the index means that Blackrock does minimal research into its holdings and makes no judgements about sustainability. They pay for that insight from third-party providers, specifically MSCI, a large provider of indices and portfolio analysis tools.

Does it say what it does?

The fund is very clear in its fund documents about how it selects assets for this fund. The index it tracks starts by mimicking the Agg. Then, where relevant, it applies MSCI’s screening and rating process to remove entities involved with “bad” industries like alcohol and tobacco, controversial weapons, and certain fossil fuels. It also sidesteps bond issuers with high controversy ratings, while overweighting companies who score well in MSCI’s ESG ratings.

Does it do what it says?

The phrase “where relevant” is doing a lot of work here. ESG screens and ratings in this fund are only relevant to corporate bond issuers. Government bonds, government-backed bonds, and other kinds of asset-backed bonds either don’t get ESG ratings or the ones they receive aren’t used in this fund’s methodology. The vast majority of any fund that is following the Agg index will be made up of these government and asset-backed securities that are included with limited ESG thought.

So, while the entire fund is labeled “ESG,” the most recent prospectus shows that only around 30% of its holdings are “subject to the Index Provider’s optimization process” – which is a complicated way to say that ESG criteria are being applied. As a result, EAGG’s portfolio looks very similar to the Agg, with just a slightly higher ESG score. The MSCI ESG Quality Score for EAGG is 6.7, while the Agg scores at 6.2 (on a scale of 1-10).

With such little difference between EAGG and the Agg, it’s unsurprising that their performance and risk metrics are very similar as well. One place where there is a difference – it’s going to cost you about 0.07% (7 bps) more in fees to choose EAGG over a comparable fund that does not use the ESG filter.

Who is this good for?

EAGG is a reasonable choice for investors who want to dip their toes into ESG-themed fixed income funds. If you want to invest in bonds to lower your risk or diversify your portfolio, EAGG provides the performance and risk profile to suit your needs. And its ESG approach is legitimate, even if it is limited. Just set your expectations that this fund isn’t all-ESG approved throughout.

The “S,” or social, in ESG is typically the most neglected of the three components that make up sustainable and impact investing. S&P Global defines S as “a company’s strengths and weaknesses in dealing with social trends, labor, and politics.” This broad definition includes a range of issues including workplace health and safety, harassment and grievance policies, wages and working hours, supply chain practices, and DEI (equality, diversity, and inclusion).

Why Is the S Neglected?

One reason is that while we now have robust metrics and frameworks to track a company’s carbon footprint, human capital management policies and procedures and the downstream effects of a company’s culture on employees are more challenging to measure and have not received the same attention as environmental factors.

The social component of ESG is also arguably the most political. If, as many traditionalists believe, a business’s sole focus should be maximizing financial returns, anything beyond that, like human rights or social justice issues, are thought to be a breach of fiduciary responsibility. In fact, we are seeing a backlash to the growing popularity of sustainable and impact investing, particularly social issues.

The June 2023 Supreme Court ruling that ended race-conscious admissions programs at Harvard University and the University of North Carolina has spurred legal attacks, or the threat of them, on corporate diversity programs. In July 2023 thirteen state attorneys general sent a letter to the CEOs of the top 100 corporations arguing that the ruling could also apply to employers. By mid-2023, DEI-related job postings fell 44% from the same time a year prior, and many businesses, including Meta and Google, were slashing their DEI programs and initiatives.As part of the contentious March 2024 spending bill, the US House Office of Diversity and Inclusion was axed.

In response to these challenges, many businesses and universities are scrutinizing their social policies and wondering whether it’s time to retrench or cut back rather than move forward. This article presents three reasons why going backwards is not a viable option and choosing to recommit makes good business sense.

Reputational Risk

One of the key drivers in the push for sustainable and impact investing has been public opinion—for example, consumers and other stakeholders who push to boycott a product or service, or post negative online reviews of a company based on its use of child labor, safety problems, or other workplace issues. For instance, S&P Global Market Intelligence found that people were more likely to shop at Walmart after it stopped selling certain guns and ammunition. Younger consumers in particular are taking a more active role in scrutinizing products and services, and can be unforgiving in how they use their purchasing power.

Trent Romer, third-generation co-owner of Clearview Bag Co, Inc. from 2000 to 2021, told me the story of how he tackled reputational risk to his family’s plastic bag manufacturing business. Concerned by the damaging effects of plastic on the environment and growing consumer outrage, Romer began to educate himself and his employees on how his company could be both more sustainable and profitable. Over five years, he and his brother restructured the company, starting with creating a recycling process that repurposed materials and reduced waste by 25%.

He introduced certified compostable materials and, together with employees and customers, created a new vision: healthy planet, healthy people, healthy company. The company became more profitable, grew overall value, increased customer and employee satisfaction, and increasingly attracted outside investment opportunities. Romer wrote two books about his experiences and advises other business owners, further burnishing the company’s reputation as a sustainability leader in a tough industry. Longer term, Romer talks about the challenges for small to midsize businesses in managing the challenges of the regulatory landscape.

Regulatory Risk

The regulatory pace for ESG disclosure is accelerating, even in the U.S., despite fierce opposition from some sectors, particularly the fossil fuel industry. In 2020, for the first time the SEC specifically addressed the social component by approving amendments to Regulation S-K. Public companies are required to disclose human capital measures or objectives related to business management, including development, attraction, and retention of personnel. The SEC has hinted that it will be looking more closely at these issues in the future.

In 2021 (and updated February 28, 2023) Nasdaq adopted diversity disclosure rules that require companies listed on its U.S. exchange to “publicly disclose board-level diversity statistics annually using a standardized template; and have, or explain why they do not have, diverse directors.”

In March 2024, the SEC adopted rules that will “enhance and standardize climate-related disclosures by public companies and in public offerings.” Required disclosure covers actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model, and outlook, beginning with annual reports for the year ending December 31, 2025.

The EU has been passing much stricter regulations over the past ten years, and U.S. companies doing business there need to pay attention. Starting in January 2025, the Corporate Sustainability Reporting Directive (CSRD) requires any EU listed company or non-listed company generating more than €150 million on the EU market or with over 500 employees doing business in the EU to report on all ESG issues.

The global ESG regulatory landscape is still fluid, varying by country and required disclosures, and in the U.S. heated controversies around regulations will continue. But it is increasingly clear that going backwards is not a long-term answer, and businesses that understand opportunity risk will have the advantage.

Opportunity Risk

Climate change, AI, pandemics, supply chain disruptions, political unrest—the global economic and business challenges are enormous, as are the opportunities. A July 2023 report by McKinsey looked at what it calls “a rapid evolution in the way people work and the work people do.” The following two findings alone should make companies and investors wake up to the importance of S: by 2030, roughly “30 percent of hours currently worked across the U.S. economy could be automated,” leading to “an additional 12 million occupational transitions,” a much higher number than projected in 2021. That means millions of workers having to switch jobs or careers, with most of the disruption falling on low-wage workers and women.

An article for the Harvard Law School Forum on Corporate Governance makes the compelling argument that companies and investors who understand how to integrate social factors into their business models and portfolios will gain a competitive advantage and be better poised to thrive in a rapidly changing global economy.

And what about younger employees—the ones who will be leading the innovation charge? Deloitte’s Global 2022 Gen Z and Millennial Survey presents a snapshot of what they want: “Higher compensation, more flexibility, better work/life balance, increased learning and development opportunities, better mental health and wellness support, and a greater commitment from businesses to make a positive societal impact.” And 52% want to see more diverse and inclusive workplaces.

In an interview I did with Anna-Lisa Miller, Executive Director of Ownership Works, a nonprofit organization that partners with companies and investors to provide all employees with the opportunity to build wealth at work, she explained how paying attention to the S can result in wealth creation for everyone. After one company offered shared ownership, the value of the business increased, employee engagement and productivity rose, and employee retention skyrocketed.

In Part 2 of this topic I will cover some of the best frameworks being used to track the S in ESG and look at how businesses are incorporating social KPIs into their overall business strategy–a crucial component in driving employee innovation in the workplace and addressing some of the most challenging issues in advancing basic human rights.

Inspired by Women’s History Month, we’re launching an ongoing interview series with top women in the worlds of finance & investment, clean technology, environment and society. These are virtual fireside chats with some of the most experienced and knowledgeable women in their industries. We’re thrilled to kick off this series with a two-part conversation with Kristin Hull, founder and CEO of Nia Impact Capital.

In Part I, we learn about Kristin’s background, which blends the worlds of finance and education, get introduced to Nia Impact Capital, and ask Kristin about the wins she is most proud of. (Read to the end, because those wins are pretty big.)

This interview has been edited for length and clarity.

Birgitte Rasine: Kristin, pleasure to have you with us for this inaugural story for Women of Impact. Tell us about the impact investment firm you run, Nia Impact Capital.

Kristin Hull: Nia is the Swahili word for intention and purpose. Our work is about harnessing financial markets for social justice as well as for environmental gains. And so that’s really where the term Nia comes in: it means purpose. Bringing that sense of intention and purpose, both to every company that we invest into and to building our own firm to follow best practices in human capital management, training young people in sustainable finance.

We build high impact public equities portfolios with intention and purpose. We design concentrated portfolios, investing at the intersection of environmental sustainability and social justice. We look across our six solution themes for companies that are going to benefit from, and help us in, the transition to a just and sustainable economy: which companies are going to play a part, which ones are poised to help in the transition and which ones are doing the very best human capital management. Currently we have $475M under management.

So that’s the product side. We have a Changing the Face of Finance internship program, which is a core component of what we do, and that’s training. It’s really making a space for young and potential changemakers to come in and learn how to do sustainable finance because there are just so few shops, firms, asset managers doing sustainable and social justice investing in an authentic way. There’s a lot of greenwashing out there and not very many people who know how to do it in a way that can actually change systems.

The other piece [of our work]—that we don’t get any revenues from, although we’re well known for it—is engaging with every company that we invest in, as part of our due diligence process. Getting to know the people behind the ticker symbol and working to make change. We know that change happens one conversation at a time and we have those conversations with as many companies as we can.

BR: How would you describe the kinds of people attracted to Nia and its model?

KH: Our clients are our investors; we work to empower them to feel that they can invest in a really competent way. Nia attracts forward thinking investors: those who care about the environment, and those who understand we are in a transition to the next, just and sustainable economy and who want their assets aligned with and benefiting from that transition.

We also tend to attract those investors who are interested in the benefits of diversity in leadership, and companies that include women in senior management.

BR: How did you originally become interested in finance? What motivated you to focus specifically on responsible or impact finance?

KH: I grew up in a trading firm. My dad started a trading firm in a garage—as one does in California—and so we were talking puts and calls and pork bellies, and commodities, futures, options, derivatives. So that’s what I was hearing since I was about 14—and not necessarily loving that [laughs]. It was a family company, and it was a requirement to work there and it was a way to connect with my dad. Later we moved to Chicago—it was summers on the trading floor and the mantra at the dinner table and the backseat of the station wagon was always, buy low and sell high, as often as one possibly can, which is what you do in a high-frequency trading firm.

I would ask questions like, what kind of good are we doing, what are we doing by being the market maker. There were times where being that middleman seemed to make sense and yet it was always very transactional. When we sold that company to Goldman Sachs, that’s when we really got to take a step back and see what was next.

By then I had started a career in education. I had started a charter school in Oakland and I was helping with the fundraising for the charter school, working with the city, with the banks and foundations to get loan guarantees. As the capital campaign came together I realized that the people in my community—the teachers and the parents—had few financial skills or aptitude. I had to do something about that. So creating products that were transparent, focused on the solutions, and meant something and were tangible to the people in my community, that’s what motivated me to create Nia.

BR: What an inspiring story—especially love hearing about your commitment to education. I imagine you put just as much thought into supporting your team. We know it’s not easy being a woman leader in the investment space.

KH: It’s definitely not easy to be a woman in finance, and to be an asset manager, where women-led firms make up just 0.7% (yes, less than 1%) of the $80T under management. Every day can bring challenges, and yet at Nia, we have built an incredibly strong and talented team. We’re thoughtful. Thoughtful and intentional. We recognize we are humans in this space—and we’re also women in this space. We’re in financial asset management, the belly of the beast, which has been white male dominated, you know, since inception. So, we aren’t just trying to build a status quo company, we want to build a company that honors individuals. Just like we don’t want to invest in companies in a transactional way, we don’t want our company set up that way either.

BR:You’ve worked on issues ranging from renewable energy to gender equality to social justice, and you’ve been able to move a few mountains in the seven short years Nia has been around. What have been your greatest gains in terms of moving the needle on large corporations?

KH: There are some big standouts. We won a shareholder resolution at IBM for enhanced diversity reporting which was really important to us because of their size and the role IBM plays in the global economy. We won with 94% of that vote, which is pretty unheard of for a shareholder resolution. The company actually ended up supporting our resolution, which then garnered more support.

Particularly with AI, the algorithms that are going to rule our world, we need to make sure that there are diverse people at those [corporate] tables. They now have a chief diversity officer and she has, I believe, 50 people reporting to her, so it’s not just a checkbox—they actually have a program and are really rolling this out. And we can check in with them on their progress. That was a pretty big win.

BR: The IBM case study is well worth a read—it makes you appreciate just how much work—and conviction—went into persuading a large corporate entity to work with you rather than against you. You were also able to make a shift at one of the world’s largest and best known companies.

KH: Yes—another win announced last year was Apple. Because of our collective work, Apple removed concealment clauses from all of their employee contracts. We got everything we wanted: US employees, international employees, and all contract workers. That was a big deal.

BR: That is a big deal—and just for our readers’ information, a concealment clause in an employment contract limits a worker’s ability to talk about any unlawful activities at work, such as harassment and discrimination. In other words, if a woman—or any person—can’t speak up about harassment or discrimination on the job, they are effectively silenced and put into a vulnerable position. Kristin, having achieved these significant shifts, what are you most proud of?

KH: I think the thing I’m proud of personally, is just our perseverance. That we’re still here and we’re still doing this. I ran into someone I knew from our co-working space over 10 years ago—she had moved away to Vermont and happened to be in town that weekend. She said, “You’ve inspired me in so many ways. I’ve watched you grow Nia from nothing to this.” I think showing other women that change is possible, that means a lot.

Join us next week for Part II, where we talk about some of the challenges in the work Kristin’s team is doing, both in the male-dominated venture world and the larger sphere of corporate influence, and how far we still have to go.

Read about another woman powerhouse, this time in the professional football arena (yes, really!)

This interview has been edited for length and clarity.

Welcome to another episode of “The Impact” on FinTech TV. I spoke to Josh Hatch, Principal & Partner at Brightworks Sustainability, about how they are assisting clients in establishing & implementing sustainability programs. We also discuss the growth of the digital economy, the intersection of ESG & AI in tackling climate change, Brightworks’ future investment plans, and the main drivers of the sustainability conversation.

Jeff Gitterman: Josh, thanks so much for joining me today. Tell me about yourself and Brightworks Sustainability.

Josh Hatch: Brightworks Sustainability has been in business since 2001. It originally started as a sustainability consulting practice and grew really fast. We got into green building work as that was one of the bigger drivers of sustainability impact for a long time. As the broader markets are catching up, we’re doing a lot more in the ESG space: helping a lot of companies both from top down corporate strategy, but also from bottom up implementation in their facilities and their policies and their supply chain.

JG: Define the difference between ESG within building spaces and sustainability—I think people either conflate the two or get the two confused.

JH: I think classically green building and sustainable buildings [means] thoughtfully designing and running buildings: it’s their energy use, energy efficiency, water materials, green cleaning products, the whole spectrum of designing and running a building sustainably. When you get to ESG, the notable difference to me is the policies, the governance, the regulation. In the beginning you had a green team, and they wanted to do things better, but eventually it grows up and then it needs policies, it needs corporate goals, it needs the level of data and tracking to see how you’re doing and eventually to roll up to investors. So it’s the grassroots growing up and becoming serious adults.

JG: And you guys take this into the space of digital infrastructure. Can you explain what got you interested in that aspect?

JH: Yeah, mostly for impact. As we’ve seen, our lives are becoming increasingly digital, professionally and personally. It’s a fast-growing sector. It’s growing a lot, it has large impact. It’s also been one of the more innovative sectors. What motivates me in my work is that we feel like we can really make a difference. They’re funding some of the more innovative strategies, and the hope is that we can socialize and spread that and democratize those solutions to all the other sectors. So it allows us to do some of the leading work and then share it with all the clients we work with.

JG: We hear a lot about the growth of the digital economy and everything else we see in the stock market, the Magnificent Seven is mostly being driven by a digital economy. Is that growth sustainable in your opinion?

JH: I think what we’ve seen over the past few decades is unfettered growth. There haven’t been that many constraints. Digital has become increasingly part of our lives in that time period, and these companies have grown exponentially. We’re now seeing there’s always been constraints, but they’re becoming much more significant. They’re running out of power, they’re running out of water, and then social pressures, both willingness to operate, where they’re allowed to develop, and I think also just competition for our time. I think people want to have digital be part of our lives and enrich our lives, but they don’t want it to become our lives. So I think that there’s pushback from an environmental standpoint, from a social standpoint, and there’s even been financial pressures on them in the last few years.

JG: So from that perspective, what role does the consumer play in driving all of this growth and demand?

JH: I think the consumer is still growing up with how much they want digital in their lives. I think we’ve all benefited—digital has made our jobs easier and our lives better, but there’s also a dark side to that, [like] the term doom-scrolling, people know now that we don’t want to be online, on-screen, all the time. It wants to help us do the things we enjoy, family, rewarding professional experiences, being out in the world, hiking, it can help all that, but it doesn’t want to become the only experience. So I think consumers are starting to moderate their use and be more thoughtful. And increasingly, the tech companies have had an unlimited mindset in terms of let’s store everything, let’s compute everything, let’s not think about what makes more sense. With these constraints, the companies are being more thoughtful about how they’re going to run that and consumers are likewise thinking about what’s most valuable to them and what’s going to make their lives better.

JG: Recently we’ve seen the hearings in Congress where all the social media companies had to talk about how much damage they are doing to kids, so I think you’re right, there is this pushback, how much does it enhance our lives, how much does it make our lives more difficult today, and people are definitely wrestling with that. I grew up without internet, when I say that to my kids they’re like, “What? How did you grow up without internet? It seems crazy.” We’re also hearing conflicting stories within AI. Thomas Friedman said in his editorial in The New York Times a few months back, “The two biggest threats to humanity are AI and climate change. The one hope is that AI will solve climate change.” So in those conflicting narratives, we’re hearing, maybe AI will provide solutions and answers and digital infrastructure will help save us. At the same time, and you mentioned this in your remarks before, we’re worried about all the demand for water and energy that is being driven by digital. How do we balance these two stories?

JH: I think that neither extreme is right. AI is not going to solve everything, but it’s also not the case that it’s good for nothing. I think there are real applications where we’re going to find that it can help in particular with the grid and energy, and it’s an inherently complex system. And as we move towards a more dynamic model where it’s not just base load fossil fuels with peak natural gas, when we’re moving into a dynamic mix of resources with intermittency on renewables and solar and batteries mixed in, that level of complexity, machine learning is going to help, but, again, it’s not going to solve everything.

What we’ve seen is that over the last decade or so, technology companies have driven a significant portion of the greening of the grid. They’ve inked half, two thirds of the renewable energy that’s privately developed. So they’ve been a big part of the solution. The question is as we move forward into the next decade with more constraints, transmission constraints, constraints on where we can develop in available sites, can they continue that innovation, can they continue to be the leading companies helping the sustainability component be fully addressed? The worry is that they will pull back from those commitments and that innovation…

JG: In order to meet demand.

JH: In order to meet demand and move back to more traditional methods, whether that’s fossils or nuclear or whatever. There are two paths here. If they continue the leadership and innovation that they have, which I’m really hopeful for, they can drive those solutions through the rest of the economy. Or if they revert to some of the historical older methods, it could be the undoing.

JG: But you’re seeing even Microsoft now launch a whole nuclear division within Microsoft to look at that. How do you feel about nuclear as a potential solution for all of this increased demand from infrastructure?